Last Updated on April 23, 2026 by teamtfl

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.” – Benjamin Graham

Here is a paradox that most Indian investors live with: they know equities have given the best returns of any asset class over any 15-20 year period. They have seen the charts. They have heard the stories. And yet, most of them have not made serious money in equity markets.

This is not because the markets failed them. It is because of how they think about equity.

⚡ Quick Answer

Equity means ownership in a business. When you buy a share or invest in an equity mutual fund, you become a part-owner of that company’s earnings, assets, and growth. Equity delivers superior long-term returns because businesses grow earnings over time. But those returns require patience – the same patience you would give your own business. Most investors fail in equity not because markets are risky, but because they apply short-term thinking to a long-term asset class.

Equity Is Ownership, Not a Price Movement

This is the most important reframe. When you buy 10 shares of a company that has 1,000 shares outstanding, you own 1% of that business. Everything that business earns, everything it owns, and every rupee it retains to grow – 1% of that is yours.

Now ask yourself: if someone asked you to become a 1% partner in a profitable business, how long would you commit before deciding whether it was working? One week? One month? Most people would say at least 2-3 years, probably 5. You would not judge a legitimate business by what happened in the first few quarters.

Yet when the same investment is packaged as a share or a mutual fund unit, investors check the price daily. They panic if it falls 15% in three months. They exit at the worst moments – market bottoms – convinced that something is fundamentally broken.

Nothing is broken. Businesses fluctuate in short-term price without changing in fundamental value. The investor who understands this owns equity differently from one who does not.

The Farming Principle

Equity follows the logic of farming. You sow a seed. You water it. You wait with patience. The harvest comes – but not on your timeline, on the plant’s timeline.

We keep gold for generations. Grandparents start fixed deposits for grandchildren. But nobody says “I’m starting an equity SIP today so my grandchildren will have a significant corpus in 30 years.” That is precisely what they should be saying. The same family that buys physical gold (which underperforms equity over every long period) will not invest in HDFC Bank or Infosys shares for their grandchildren’s education – even though the businesses they would be owning are far more likely to compound wealth over 30 years than any yellow metal.

The question is not whether equity will work. The question is whether you will stay invested long enough for it to work.

RetireWise builds retirement plans that use equity as the primary long-term wealth-building tool – with the right allocation, the right funds, and the right behavioural framework to stay invested through every correction.

Speculation vs. Fundamental Investing

Equity delivers two types of return. Speculative return comes from short-term price movement – buying at Rs 100 and selling at Rs 120 within weeks. Fundamental return comes from business growth – the company earning more, expanding, and retaining earnings that compound into share price over years.

The vast majority of Indian retail equity investors are seeking speculative returns. They time the market instead of giving time to the market. This is the primary reason the average Indian equity investor consistently underperforms the index. The Nifty delivers 12-13% CAGR over long periods. The average equity mutual fund investor in India has earned significantly less – because they buy after rallies and sell after corrections, systematically reversing the buy-low-sell-high principle.

Fundamental investing requires a different mental posture. You buy businesses you understand. You hold them long enough for the underlying earnings growth to translate into price appreciation. You ignore short-term price movements as noise. You do not check the portfolio daily.

What Risk Actually Means in Equity

Most Indians say equity is risky. They are not wrong – but they mean the wrong kind of risk. In the short run, equity is volatile. A portfolio of Rs 10 lakh can become Rs 7 lakh in a year. That volatility is real and uncomfortable.

But the real risk in a 20-year retirement plan is not short-term volatility. The real risk is the erosion of purchasing power over time. A fixed deposit earning 6.5% when inflation is running at 6% is delivering near-zero real return. An endowment plan returning 4-5% is delivering negative real return. These instruments feel safe because the rupee balance does not fall – but the purchasing power of that corpus is being silently destroyed year by year.

Equity, over any 15-year rolling period in Indian market history, has delivered positive real returns – returns that beat inflation. This is the correct long-term risk comparison: not “will my portfolio value fall this year” but “will I have enough purchasing power in 25 years to fund the retirement I want.”

Why People Don’t Make Money in Equity

The Nifty 50 has delivered approximately 12-13% CAGR over 20-year periods. Yet the average equity investor in India has earned considerably less. The gap is explained entirely by behaviour: greed near market peaks, fear near market bottoms, and the resulting pattern of buying high and selling low.

The investors who did make money in equity over the last 20 years are not the ones who correctly predicted every correction. They are the ones who stayed invested through every correction – the March 2020 crash, the 2018 NBFC crisis, the 2015-16 correction, the 2011 fall, the 2008 global crisis.

Each of those events felt like the world was ending when it was happening. Each of them was a buying opportunity in hindsight. The investors who understood that equity means ownership in businesses that would eventually recover and grow – those investors are wealthy today.

Read: Should You Invest in LIC IPO and Other IPOs?

Equity works. The Indian economy has grown, is growing, and will grow. The businesses in the Nifty and Sensex will earn more in 2035 than they do today. The investor who owns them patiently will share in that growth. The investor who trades them nervously will not.

Time in the market. Not timing the market.

Is your equity allocation sized correctly for your goals and timeline?

RetireWise builds goal-linked portfolios where equity exposure is calibrated to your specific retirement timeline, risk capacity, and required return – not a generic allocation.

Your Turn

What was the moment that shifted your understanding of equity – from “risky” to “long-term ownership”? Or if you are still hesitant, what specific fear is holding you back? Share in the comments.

Great explanation! To all my friends who are willing to invest in equity MFs and don’t know which fund to pick. I’d strongly suggest to avoid taking advice from any friend or stranger as the fund selection depends on your risk appetite (how much risk can you bear), your investmind duration and other factor. Since you are already interested in understanding equity, I’d rather suggest to gain more knowledge about types of mutual funds and improve your financial IQ as that’s going to help more in long term.

Hi sir, I am Bhargavi I am just planning to invest money equity with mutual fund is okay to invest?

if i want to invest on which i can invest can you help me sir?

Amazing explained ?

Thanks Abhilash 🙂

Superbly explained sir ..jo topic aj tk smj nhi aya ek br m aa gya ..

Easy to read and understand..

Your style of explaning is awesome ..

Thank u so much sir

Useful

Thanks 🙂

Hello sir,

I am 25 years old now, i am planning to save 5000 rs per month to get best returns in future, please suggest me which is the best plan??

Good article to make people understand about equity. What I observed on some of my friends is they don’t know the mutual fund name also. When asked they only answer the AMC name, not the total name of the fund. They bought the fund mostly on the friend’s suggestion that the fund is doing good.

Hi Suman,

It’s really dangerous to give or take financial advice from friends 🙂

Nice

Dear Sir,

I am 44 year old marketing guy. To avoid IT i have invested 1 lakh rupees in Insurance in the last 5 years. After maturity i was surprised that i didnt expect the returns what they have promised. So friends advised me to invest in mutual funds. I am not a finance guy.

kindly suggest best advise whether to invest in mutual funds/trading.

Warm regards,

sampath

Hi Hemant

It is not only greed and fear, its lack of patience also.

and you can not keep watering a plant which is not growing. I think you should have some exit strategy also.

hello sir; I am a govt employee I want to invest some money in mutual fund.. I have consulted with many others about equity/mutual fund/sip also bt many of their ans are differnt .. I m looking for some best funds whr I invest my money for my better future plss. Suggest me about some of best return fund. I have already opend a sip of rs 500p/m. I wnt invest more for long term. Thank you..!!

Sir as an agriculturist I tend to earn an official income of 6 lakhs per annum. Excluding the expenses, what is the maximum amount I can invest in each individuals of PPF, SIP, and Equity funds(ELSS fund, or other funds) each year in order to exempt maximum taxes (I know agricultural income is non taxable)and gain more incomes in the long run say some 15-20 years. Please suggest me the amounts I have to invest in each funds.Thank you in advance.

Hey can you Please teach me about foreign equity what are the risks in that.

What is mutual fund ? How can i invest in mutual fund?

can i make monthly income with equity

Sir I want differences between preference share & equity share.

Hi Hemant,

Thanks for the TFL. I am a fresher who started job in July 2014. TFL has done good work in spiking my interest in financial matters. As far as I understand equity is a better option for safe and high returns. But what I don’t know is where exactly to start? I am actually troubled by the thought about how do I start investing? Could you please share some thoughts on it?

Sir i have just starting to educate myself in finances and therefore asking u a very basic question

1▪ In Equity mutual funds do i have to invest a capital just once or monthly for a particular share ?

2▪ Do i have to specify right in the beginning the period for which i want to hold the share or it is my wish n will to withdraw whatever money has been made yet?

3▪ what is the smallest amount i can invest?

Dear Hemant

Thank you for this nice post. I am new to the world of investment and currently going through your “financial literates” modules. I understand from your previous comments that investment in equities require a lot of market research and dedication. Naturally it is very dangerous to invest in the equity markets just on a whim or without proper and diligent research. So i want to ask if it is possible to make our investments through some investment managers or dedicated brokers? And how to go about it? I shall be obliged if you reply in kind.

hi

i started with Rs 2000 sip each in HDFC top 200 and IDFC equity for 24 month . my time period for sip is completed in June 2013 and did not book it to liquefy it.and i want to restart it for a period of 10 years.how can i do it

secondly,is it possible to invest one lacs rupee onetime in mutual fund equity ,if yes then how.

Dear sir,

I want to invest 2000 pm in SIP. Suggest me the best mutual funds.

Hi Sumeet,

Read here

https://www.retirewise.in/2013/01/best-mutual-funds-to-invest-in-2013-india-top-schemes.html

Hi Hemant,

I have a doubt…

As you said in the article that if one invests in the equity of a company he owns a portion. Now if that company register profit they’ll distribute the dividend to its shareholder. It means better the company, better will be the profit and so will be the dividend. However as i feel the return which shareholder gets, is mainly due to price appreciation of the company’s share, dividend portion is not too significant. Then why one should invest in a company which will make good profit instead they should invest in a company whose share price appreciation possibility is high. Assuming a situation where lot of people are buying shares of a small company then if company register loss in business then also invester may get good return because of price appreciation.

I am a layman in this field and it may be clear from my question 😐

Hi Swapnil,

Price appreciation is a major reflection of the company performance. Any company which is distributing its surplus to the shareholders in the form of dividend is considered to be good cause it can happens only when the company is generating good profits. Its only in the initial stages when the company requires higher capital for expansion that they may utilize the surplus for this objective. But if any company is incurring losses for sometime and the price appreciation is still happening then it is not reflecting the true picture of their performance. The company might be in a huge debt then how come it can give you growth? Think of real estate …..it was the same story…company not generating profits…going in huge debt…still share prices were rising….finally they corrected but investors lost….

I hope this answer your query….

Hello Hemant;

Nicely wrote! But can you answer this question?As you wrote for the long time but at that time many basic things were not present in India like cell phones,infrastructure etc.Again we saw IT share given MINNDBLOWING returns .Now the thing is does our economy really have capacity to grow the rate equivalent to past rate ?There is big problem of government policies also.

Sencond thing every after 2-3 years there are sign of “Mandi” in a fast growing economy like India what this indicate?

My third question is in last 5 years only 3 mutual fund(Diversified equity fund) managed to give returns more than FDThen answer me why should an investor look for equity?

Hi Mandar,

I will not go for specific sectors but the answer to your question is that when we are assuming equities will not perform in the long term then we are also assuming that companies will not do business or if they do then they will not be able to grow. That’s probably a difficult scenario.

Second is the long term investment. If you hear recent stories then there are investors who have held their equity investment, primarly stocks, for 15-20 years and now reaping the benefit of earning high dividends in their post retirement years. They have witnessed so many cycles of ups and down but never liquidated their investment. The primary reason for this is that they invested in companies who have grown from small to big and so their investment. Some of them may not have yielded good result but the performers negated the under-performance of these. Ideally, that should be the long term investment. You have to give enough time to your investment to grow. Yes the cycles of market under performance at different times can vary due to different reasons but we need to consider a long term investment from a long term perspective.

I hope this answers your queries.

Dear sir,

I am a new in mutual fund, i want to know can I open equity mutual fund through online?please give some reliable links by which I can invest in equity for long term.

Hi Arnab,

Yes you can invest in equity mutual fund online either through respective company website or through online intermediaries. Even MF distributors will also give you option for investing online but you will have to go for one time registration which will require some paperwork to do.

Hello Sir,

I want to invest in market. I m fresher in this field. So please guide me that how to open DEMAT account (with whome i.e. Religare, SBI, ICICI) and where to invest (Eqity, Commodity etc.).

Hi Yatin,

Th below article will give you some insight on what strategies you should adopt for investing.

https://www.retirewise.in/2010/12/investment-young-people.html

hi hemant

my name is bhanu iam working with a animation studio and earning 12k per mnth. there are no savings done so far…but i want to invest for future plz tell me where to invest.is mutual funds give gud results in4-5 years…

Hi Bhanu,

Mutual Funds are ideal avenue for accumulating through monthly savings.You can create a good portfolio through your investments.

For knowing more read here

https://www.retirewise.in/2011/07/best-mutual-fund-for-sip.html

Hi Hemant!

I’m reading your articles for a few days and now I’ve subscribed for tfl guide newsletter. You are really doing a great job to helping people like me to understand the market.

I’m a person with a small monthly income of Rs 13000. I want to invest in Reliance Equity Opportunity Mutual Fund through an SIP of Rs. 500. My time horizon is for 12 years.

Will it be OK or any other fund you would like to suggest?

Thanks and regards,

Ramanuj Singh

Hi Ramanuj,

You can read this to know more:

https://www.retirewise.in/2011/07/best-mutual-fund-for-sip.html

Hello Hemanth,

My name is Venkatesh and I am a BE, MBA graduate with experience of more then 5 years in the Business Development hood under the IT sector. Currently I am a freelancer and consulting few companies regarding the business process modelling. I am planning to be a investor and make this as my full time job.

Please suggest me if inter day trading is more effective or carrying it for more then one day? All I am looking at is making the profit of 10% and in the short run (Max 25 days). If you have any other investment plans please guide me through. Thank you in advance for your time and patience.

Regards,

Venkatesh P.S

Hi. sir I m so glad that i found you. wel i m 25 yr N completed my MBA i am moving myself in share market to work as wel as to know about it. please help me i want to know from begining what is share? And what is share market. i m glad if you will help me.

Hi Raj,

Read some good books and you can go for NCFM exams from National Stock Exchange to get yourself aware about stock market and its working.

Dear Sir,

I am of 30. what is the best pension policy?

when should I start investing in same.

Hi Himanshu,

You are at a good age to start accumulating for your reitirement. Pension policies have not been able to deliver and some strict IRDA regulations has made them least attractive.Also traditional and ULIPs pros and cons are there to consider. You can think of investing through Mutual Funds which are highly liquid and cost effective instruments to invest for retirement.

sir

what is mean by equity broking ,what are the content involved in equity broking,and what should we understand from “investers preference towards equity broking”

hi hemant sir,

presently i am working in siemens as a design engineer, i am very much itreseted in share market in nse, i want to be a sub broker, nse module capital market dealer module i have is it sufficiant for sub broker exam & i want to ask u one more think that a lot of nifty is better or any indiavidual company share. & if i am purchasing any share of company than that time whats thing i need be calculate

every month i can save upto 5k upto 11months time. can u please suggest me .where i can invest so that i can get my money with minimum back .on 12th month iam planning to take insurance plan with that money ..

please suggest me as early as possible ….

Hi Ravi,

I think you should read – What is Insurance

https://www.retirewise.in/2010/04/what-is-insurance-investment-or-expense.html

well explained

Thanks 🙂

Hi Hemant,

It has been a pleasure for me reading through the articles at http://www.tflguide.com. Its rightly said by you that investing directly into equities demands greater attention and also some disciplined approach towards it.

I’m 24 years old, a software engineer by profession, just 2 yrs into job. I have keen interest in equities and try to follow up with market scenario as much as possible. Its quite a daunting task to invest in equities and earn regular returns. I have invested and have faced the music couple of times, though I would like to continue and learn on the job. As rightly said by you, one can invest in Mutual Funds if one has zero knowledge of equities.

I would like to invest in some good funds – monthly 10,000 for a period of 7-10 yrs which would give me an avg. annualized return of around 20-25%.

Can you suggest some funds which I can consider, some balanced fund through which I can achieve my goal. I prefer HDFC as a Mutual Fund House over others.

Hi Sapatarshi,

You can start with HDFC Prudence Fund.

Hi Hemant

The equity fund comes with 3 option- Growth, Dividend payout and dividend reinvestment.

Which one is better one and with what implications.

Thanks

Sumit

Hi Sumit,

Have you checked the latest article on mutual fund questions.

Cudos Mr. Hemant,

I am a Doctor and i am really impressed by the effort and heart you have put down in your website and its articles. I have not found any BETTER, STRICTLY TO THE POINT, FINANCIALLY SOUND and most importantly HONESTTTTTT articles than yours. I heartily appreciate your work.

As you have mentioned, Honesty is an important quality of a financial planner. i found out a lot of honest and hearty efforts here.

thanx for making up this site for commoners like us.

i am a 28 yr old married common man with little or no financial family liabilites. i am working as a lecturer with a monthly income of Rs. 40,000 and my parents are well to do. i’ve not managed my funds except last minute ELSS buying for tax savings. what do you suggest me to read and follow to make extra income and pension. i dont need any insurances, i have enough. i have downloaded yr ebook and will read it.

thanx for everything

Thanks Arpit. If you think TFL is helping you – must share it with friends.

Start SIP asap & also read strategies for young people

https://www.retirewise.in/2010/12/investment-young-people.html

Hope you have right type of insurance 🙂

https://www.retirewise.in/2010/12/psychology-indian-life-insurance.html

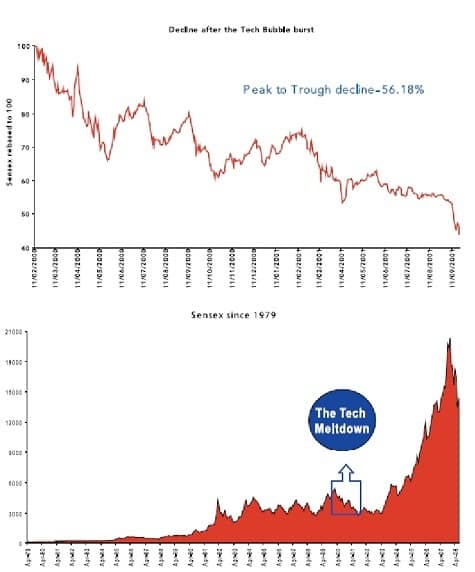

hi sir wat will happen if v r caught in spiral like japan ie correction of 80% & still bleeding though japan s co.s are not bleeding then y the nikkei is not giving the returns.i hope u must be getting wat i wanted to ask..pls do clarify why we will go on making new highs on index although with ups n downs… thnx

Hi Amish,

There are 2 reasons for what happened in Japan

First when their market topped it’s valuation was almost 5 times of average.(Their PE was approximately 100 at that time) Read below article to understand PE

https://www.retirewise.in/2010/11/sensex-pe-ratio.html

Second Japan is now a developed country & in last 2 decades their GDP growth is 2-3% max.

Hope it answers your concern. Next 10 year will be Golden years for India – you will like to sit out & watch the game or would you like to participate. 😉

hi sir,

I want to learn technical analysis and value investing concept Pls suggest some good booka and website . I have litlle bit idea about technical analysis. How to select good company & stock? Pls guide me.

Hi Jayesh,

It’s good to learn but what we want to learn is equally important. If you would have asked me about personal finance books – I would have happily shared that & that were of real use to you. Technical analysis creates an illusion that we will catch the tops & bottoms – I am not convinced about this concept. If you are really serious about reading value investing – try Intelligent Investor & Security Analysis by Benjamin graham. In these books data used is of USA but investment concepts remain same across the world. As you have asked how to select good company or stock – not for a second I ever felt that I can beat fund manager so I never tried it. When we have professionals that can manage our money for some small fee – why you want to jump directly in the market. End of the day most important thing is achieving goals or building wealth – rather than how we do it.

Read this

https://www.retirewise.in/2010/05/keep-it-simple-while-investing.html

@Hemant

I want to invest 24,000 annually to get money after 17 yrs for my daughter’s studies. She will be one year old in January 2011. Should I invest in any Child insurance plan or in a Mutual Fund. Which plan (traditional or ULIP) will deliver me highest and safe return for my daughter’s education?

Hi Atul we have always said Insurance should not be purchased of investment purpose. My suggestion is you should buy a term plan for yourself & take sum assured close to 10 times of your present income. You are asking for 2 opposite things highest & safest returns. With high returns there is always a risk of volatility. Actually in equity risk of volatility reduces with time & much better returns can be generated. You should invest 18000 in Equity Diversified Mutual Fund & 6000 in PPF Account. For Mutual Fund you can choose DSP Top 100 Fund & Templeton Growth Fund. If we expect a return of 12% in next 17 years your portfolio value will be close to Rs 12 Lakh but if you invest it at 8% you portfolio value will be 8 Lakh.

Sir i am engineering student and i want to invest in the market but i dont know how to get started so can you please help me out?

Hi Visnu,

It’s a good move that at the time of college you are planning for investment. For you this is a great time to learn about money through small investments & then make some serious investments when you start earning. Best way to invest in equity markets will be through Mutual Funds. For retail investor SIP (Systematic Investment Plan) is the better way to start the Investment because it reduces market volatility & generate higher returns with the magic of Power of Compounding. There are funds which have sound track record like you can choose any one of them to start with.

Hi Hemant

I am a house wife want to invest in share marett. How should I begin?

Hi Jyoti

What I can infer from your question is you are a non earning member & would like to trade in equity and earn some money. If trading was so easy everyone would have been rich, trading is a not a number game it’s a mind game. For retail investor success in trading has a very low probability. Read what Rakesh Jhunjunwala said on this diwali, He begs retail investors not to trade in the equity market, “I think 98% of retail people lose money in trade. Whether correction – no correction, bull phase – bear phase. Everyone has a sad story. I have traded because it’s my 24 hour profession and I am doing it for the last 25 years. Trading goes against basic human nature. You have got to die 1000 deaths and 1000 egos in order to be a good trader. It’s not easy for every human.” Instead, he says, one should invest in mutual funds. My personal suggestion is if you seriously want to contribute to your family’s income join some part-time job or work on any existing hobby that have some potential to generate money.

Hell sir .i am teachar and i want invest 2000 pm in equity by mutal fund sip for long term more than 10 year .which fund better for me. I thiknk invest 500 in 4 fund . My one Question is .for example i get 100 units per month by investment in sip after 10 year i have xyz unit . How any one loss its principal amount ? Then we have unit .

Hello sir i am new invester in sip or equity .i am teachar and i want invest 2000 pm in equity by mutal fund sip for long term more than 10 year .which fund better for me. I thiknk invest 500 in 4 fund . My one Question is .for example i get 100 units per month by investment in sip after 10 year i have xyz unit . How any one loss its principal amount ? Then we have unit . Plz reply on my email id at

Dear Mohsin,

as per My perception you have to start with 1000 Rs. sip in funds

one is Hdfc top 200 and another one frainklin bluechip fund

this fund is performing well and consistent.

or

you will go for Hdfc top 200 and franklin PE ratio fund which is balanced category fund.

Best of luck and keep a safe & regular investment(saving)

Harshit Soni

Hi sir .i am new in mutal fund sip i want to know how we lose amount in equity if we have UNITS if we dont sell .if company in loss how we lose our princ amount ?

Hi Mohsin,

Till you are not selling your Units the loss is notional. Its only when you sell you actually book your losses.

I want to invest 2 lac in share market for 10 year please suggest me best shares?

Hi Vardhan

There is one good thing & one bad thing about your question. Good thing is you want to invest for long term in equity but bad thing is you want to invest directly in equity rather than going through Mutual Fund Route. The biggest problem with direct equity is that a very small number of people can do it right. And people who can do it right don’t ask for suggestions or tips – they just research & make their investments. But most of the people just feel they’re right, till they get really screwed big time when market makes a tern. I am having a big confusion that why people think they can beat mutual fund managers? Direct equity demands too much attention & at times it’s too addictive. And when you can’t control yourself, it can ruin your portfolio and wipe out your savings. But if you still want to test the water try this with small amount.

sir

i happen to read the article and it is in simple fluid style and make common man

understand the word equity. but still i have a doubt as a layman who do not

have any qualified knowledge or expertise in investments in stocks or mutual

funds.

as a commerce graduate and as an experienced banker i have gone through

the motions of balance sheets and its stakes of different people of the balance

sheet. ie as financier, sundry debtor, sundry creditor, and as promoter of the

company. in a particular period of time. and also have gone through the reports

of the company to its shareholders. and also the reports of the auditors of the

company. and if we analaize the 2 balance sheets of the company we can have an idea of roi to various stake holders. but i am unable to know how the mutual

funds and stocks give the return. or declare dividend. and the growth shown

by your chart is alarming considering the total growth of the industrial sector.

and please guide me whether the growth shown by you can be realised.

let us imagine a stage that on redemption of equities of a particular company

whether we will all get the return shown by you. how is it possible. kindly

also tell me that the returns given is based on the profit earning capacity of the industry. or manipulation. is stock market is on scientific terms or speculative

terms.

kindly brief me about sensex and nifty and their real effect on the industry

Hi Srinivasan,

I must say you are a rare breed who can understand companies reports to check ROI.

Read this “How mutual Funds work” it may answer few of your questions

https://www.retirewise.in/2010/05/how-mutual-funds-work.html

Ya you rightly said charts are alarming & you will be surprised that we have not included dividends in it. It’s a high time people should understand right meaning of equities & should participate in growth of the economy.

Real important question “whether the growth shown by you can be realised.” I think last para answers this question.

For rest of your questions read this

You shall be surprised to know that the combined earnings of Sensex companies in 1992 was 80, in 2000 was 240 & now 860. This EPS growth directly convert into growth of Sensex from 1992 (Sensex was close to 2000) till today EPS has grown 10 times & our Sensex has grown same 10 times. Now Indian businesses are growing and so as the profitability of the companies. In this case, EPS is bound to go up and so as Sensex.

https://www.retirewise.in/2010/11/sensex-pe-ratio.html

If you still have some question please feel free to ask.