Last Updated on April 24, 2026 by teamtfl

A client at 45 once told me he would “start seriously investing” in five years, when his home loan was paid off. He expected to retire at 60. That gave him a 10-year serious investing window.

I showed him a single calculation. If he invested Rs. 50,000 per month from 45 to 60 at 12% CAGR, he would accumulate approximately Rs. 2.5 crore. If he had started the same SIP at 35 and continued to 60, the corpus would be approximately Rs. 9.4 crore – nearly four times larger, from twice the investment period. The extra Rs. 3.4 crore in difference was not from investing more money. It was from giving the same money more time.

The Rule of 72 is the simplest tool for understanding why time matters more than amount in wealth building.

The Rule of 72 in One Line

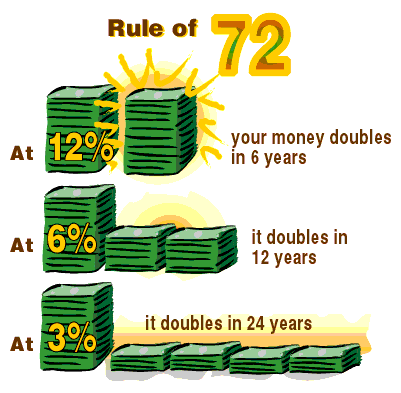

Divide 72 by your expected annual return rate. The result is approximately how many years it takes for your money to double. At 6%: 72/6 = 12 years to double. At 12%: 72/12 = 6 years to double. At 8%: 72/8 = 9 years to double. Simple. Powerful. Almost never used by the people who need it most.

The Rule of 72 Applied to Your Retirement Corpus

Here is what the Rule of 72 tells you about common Indian investment instruments in 2026.

A bank FD at 7% doubles in approximately 10.3 years. A PPF account at 7.1% doubles in approximately 10.1 years. A balanced advantage fund averaging 10% doubles in approximately 7.2 years. An equity mutual fund averaging 12% doubles in approximately 6 years.

Now apply this to retirement planning. If you have 20 years to retirement and a Rs. 50 lakh corpus today:

In an FD at 7%, it doubles once in 10 years and would be approximately Rs. 1 crore at year 10 and Rs. 2 crore at year 20.

In equity at 12%, it doubles every 6 years – so it doubles approximately 3 times in 20 years: Rs. 1 crore at year 6, Rs. 2 crore at year 12, Rs. 4 crore at year 18, approximately Rs. 4.8 crore at year 20.

Same starting amount. Same 20-year period. The difference between 7% and 12% annual return is a Rs. 2.8 crore gap at retirement – not from any additional savings, purely from the difference in compounding rate.

The Reverse Rule of 72: What Return Do You Need?

The Rule of 72 works in reverse as well. If you want to double your money in a specific number of years, divide 72 by those years to find the required return rate.

Want to double your corpus in 10 years? You need approximately 7.2% annual return. In 8 years? Approximately 9% annual return. In 6 years? Approximately 12%. In 4 years? Approximately 18% – which means taking significant equity risk or being in a exceptional bull market.

This reverse calculation is useful for setting realistic expectations. The investor who wants to “double their money quickly” in 3 years needs 24% annual return – which requires taking enormous risk, not following a sensible investment plan.

The Rule of 72 and the Cost of Delay

The most powerful application of the Rule of 72 for retirement planning is understanding the cost of delaying the start of investment.

At 12% CAGR, money doubles every 6 years. If you start investing at 30 with a lump sum of Rs. 10 lakh, it doubles to Rs. 20 lakh by 36, Rs. 40 lakh by 42, Rs. 80 lakh by 48, Rs. 1.6 crore by 54, and Rs. 3.2 crore by 60. Five doublings over 30 years.

If you start the same Rs. 10 lakh at 36, you only get four doublings by age 60: Rs. 1.6 crore – exactly half the outcome of the person who started 6 years earlier. The 6-year delay cost Rs. 1.6 crore in final corpus from a Rs. 10 lakh starting investment.

That is the mathematical reality behind the advice to start early. It is not a platitude. It is the Rule of 72 in action.

Rules 114 and 144: Tripling and Quadrupling

The Rule of 72 has siblings. Divide 114 by the annual return rate to estimate how many years it takes for money to triple. Divide 144 to estimate the quadrupling time.

At 12% CAGR: money triples in approximately 9.5 years (114/12) and quadruples in approximately 12 years (144/12). Over a 30-year retirement horizon, a 12% return produces not 4x but approximately 29x the original investment – which is what makes starting early and maintaining equity exposure during the accumulation phase so critical for Indian retirement investors.

What the Rule of 72 Does Not Tell You

The Rule of 72 is an approximation tool for compounding mechanics. It assumes a constant annual return, which no investment actually delivers. In reality, equity returns vary significantly year to year – some years +40%, others -30%. The 12% average is the long-run result of those volatile years, not a smooth doubling machine.

This matters particularly for retirement investors near withdrawal: the sequence of returns risk (getting large negative returns early in retirement) can significantly impair the Rule of 72’s theoretical outcome. A 30% fall in year 1 of retirement combined with regular withdrawals produces a much worse outcome than the Rule of 72’s smooth doubling would suggest.

Use the Rule of 72 for goal-setting and motivation – to understand why starting early and maintaining equity exposure matters. Build the actual retirement plan around a proper bucket strategy and stress-tested withdrawal rates.

A Retirement Plan Built Around Your Compounding Timeline

RetireWise builds retirement plans that use the mathematics of compounding strategically – including goal-based asset allocation, equity exposure calibrated to your timeline, and withdrawal planning that protects the corpus from sequence risk. Explore how we work.

One question for you: At your current savings rate and expected return, approximately how many years does the Rule of 72 say it will take for your existing retirement corpus to double? Does that timeline match what your retirement plan requires?

hey,its superb way of explaning thumb rules of financial planning

You wrote this article in October 2012. I just read it (April 2014) It is a really nice article. The power of compounding does go a long way!

Nicely articulated with good illustration on the rule of 72.

Sir,

Iam 50 years old and a senior PSU employee. Is am i too old to start financial planning ? Is it possible to manage my finances at this age along with retirement plans and insurance requirements and other goals as i will retire at 60years. I hope you understand and guide me. I am totally confused.

Hi Srinivas,

You should check these videos.

https://www.retirewise.in/2010/11/financial-planning-retirement-planning-guide.html

thank u, ur sir, very very nice.

Hi Hemant,

Thanks for this article. I increase my knowledge by your articles. . i m a govt. employee as a electrical engineer & my salary is 5.0 lacs/yr. now I want 2 share my portfolio. Please guide me if there r any mistake.

My portfolio as:-

1.Each Rs. 1000/- SIP in HDFC TOP200 , ICICI BLUECHIP & HDFC PRODENCE FUND & 500/- HDFC GOLD FUND. (Total SIP Rs. 3500/- per month).

2. Approximately 8000 in HDFC TAX SAVING FUND yearly in lumpsum

3. Rs. 1000/- RD for 10 year term with 9.5% interest rate.

4. Rs. 30000/- to 50000/- in PPF Account.

5. I have a term plan 25 lacs in Birla Sun Life.

6. Approximately 40000/- CPF deductd by my employer.

will be waiting for your help.

Hi Avi,

You have a decent portfolio and well diversified. However, good to analyze your requirement first so that you can align these investment with specific requirements.

You can look at increasing your insurance coverage to about Rs 50 -60 lakh.

Beautiful article.

Hi Sir, Every articles of yours are worth reading. But here im stuck with Where to start. Sir, is it wise and advantage to do SIP in MF for a term of 10-15years through portals like fundsindia.com or fundsupermart.com? Or to follow each AMC for each fund?

I’d notice less fees and convenience in privately owned portals like fundsindia.com or fundsupermart.com.

Sir, i need your suggestion Please.

Happy Diwali……

Hi popo,

Funds India a good platform for investing. With AMC you will have to do it seperately and then manage your portfolio. But with online option available with them now it should also be convenient. Avail which is more comfortable to you.

Hello Hemant,

Great Article. Thanks for Sharing Facts in a simple Way…

Well written…loved reading this article.

Sir, very very nice…..But also please infrom where can we get 12 % interest P.A , it is through SIP or Debt market which is the best investment plan, so we can get the 12 %

But Hemant considering inflation @10%…todays Rs 1000 would be equivalent to Rs 1.6 Lakh 54 years down the line..if i have calculated rightly!

Hi Amit,

Fully agree with you but does that mean someone should not save or save more 🙂

g8 job hemant ur articles are superb

very good for common man to look for

finances rule 72 ,114,144 are g8 to understand

power of compounding.

Hi Hemant

Never thought, mario can be explained in such a beautiful way. Although i have played it throughout my life, but still loved the way,you have explained it.

Mario graphics used here is superb way of explaning thumb rules of financial planning

The best part about reading your articles is – each and every word enhances my interest in investments and learn more about the ways I can invest.

Thanks for this one. 🙂

It’ll take 55.38 years for India to cross 200 Crores & 144 years for China…

what about rate of death in India VS China 🙂 ?

Super-like! The way the common “rule of 72” is explained with examples and graphics,it is bound to hold the interest of readers and is also very easy to understand for non-finance people.

Too Good. Thanks for sharing it..