Last Updated on April 22, 2026 by teamtfl

“Tell me, what is it you plan to do with your one wild and precious life?” – Mary Oliver

I once met a senior executive – let us call him Vikram – who had everything that looked like financial success. A Rs 12 crore net worth. A bungalow in a good Bangalore locality. Two children in top colleges.

He came to me not for investment advice. He came because he was confused. He said: “I have everything I planned for. Why do I feel like something is still missing?”

When I looked at his plan, I understood the problem immediately. He had planned extensively for Level 4 of Maslow’s hierarchy. He had barely thought about Levels 1 and 2. The pyramid was being built from the top down.

⚡ Quick Answer

Maslow’s hierarchy maps directly to financial planning: physiological needs (emergency fund, term insurance), safety needs (health insurance, income protection), social belonging (family security, estate planning), esteem needs (retirement corpus, wealth accumulation), and self-actualisation (purpose-driven wealth, legacy). Most Indians spend nearly all their attention on levels 3-4 while levels 1-2 remain poorly addressed. Build the base first.

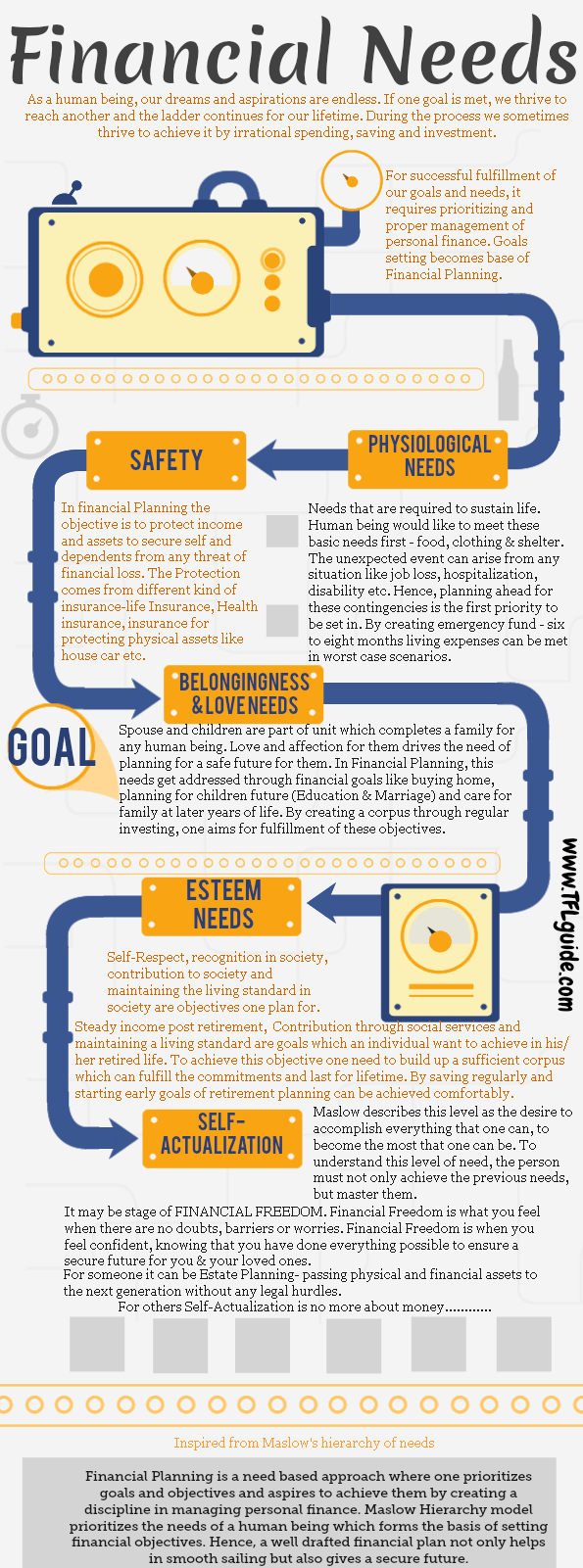

What Maslow Tells Us About Financial Priorities

Abraham Maslow’s hierarchy proposes that human motivation follows a sequence. You cannot genuinely pursue higher-order needs until lower-order ones are reasonably satisfied. The pyramid is familiar: physiological needs at the base, then safety, love and belonging, esteem, and self-actualisation at the top.

The financial parallel is not metaphorical. It is operational. Most Indian families invest for Level 4 goals (the retirement corpus, the children’s education fund, the investment property) while Level 1 and Level 2 protections are incomplete. This creates a structural fragility that looks invisible until something goes wrong.

Vikram had no term insurance. His health cover was an employer policy that would lapse on retirement. His emergency fund was three months of expenses in a city where a hospitalisation routinely costs Rs 5-10 lakh. The pyramid was visibly top-heavy.

Level 1: The Financial Foundation

Physiological needs map to the most basic financial instruments: an emergency fund, term insurance, and basic health cover. These are not glamorous. They do not grow your wealth. They prevent your wealth from being destroyed in a crisis.

For a senior Indian executive, the emergency fund question is not “should I have one” but “how large.” The standard 3-6 months advice is designed for salaried employees with predictable income and minimal family medical complexity. For a 50-year-old with ageing parents, a dependent spouse, and a child still in college, 9-12 months of total household expenses is a more realistic floor.

Term insurance at this level is not optional. A Rs 1 crore term cover bought in your 30s at Rs 8,000-12,000 per year is one of the highest-value financial purchases available in India. Many people skip it because it pays nothing if you survive. That is precisely the point.

Level 2: Safety and Income Protection

Safety needs translate to health insurance, disability income protection, and a basic written financial plan. Health insurance is where I see the most consistent gap among Indian executives.

An employer-provided health policy is a liability disguised as a benefit. It covers you while employed. The moment you retire or change jobs, it lapses. A personal health policy, bought while you are healthy, is what survives job transitions and retirement. Many executives only realise this when they retire at 58 and try to buy individual cover to find premiums that are 3-4x higher.

Buy your personal health policy in your 40s. The premium difference is significant. More importantly, conditions that developed in your 40s will have cleared their waiting period by your 50s if cover was in place early.

The Financial Safety Floor for Senior Executives

For a senior executive family in 2026, the minimum financial safety floor looks like this: 9-12 months of household expenses in liquid instruments, personal health insurance above Rs 25 lakh sum insured, term insurance equal to 10-15x annual income, and a registered will with updated nominations across all accounts and policies. This floor typically requires Rs 50 lakh to Rs 1.5 crore in liquid and insurance instruments. Once it is in place, the risk calculus for everything above changes completely.

This is Maslow’s physiological and safety base. Build it before allocating more to the farmhouse.

Level 3: Social Belonging and Family Security

The third level maps to financial planning for the family unit: adequate protection for dependents, estate planning, and ensuring that the family’s financial life can continue without disruption if the primary earner is unable to contribute.

This is where wills and nominations become essential rather than optional. A family whose breadwinner passes without a registered will and updated nominations faces months or years of legal complexity at the worst possible time. In India, this is still dramatically underaddressed. Most people I meet have neither a will nor coherent nominations across their various assets.

Level 4: Esteem Needs and Wealth Accumulation

This is the level where most financial planning attention sits. The retirement corpus. The children’s education fund. The investment portfolio. The SIPs running for a decade. These goals matter deeply – but they are the fourth priority, not the first.

The tragedy I see repeatedly: a client has built Rs 3-4 crore in mutual fund investments. They have no personal health insurance. They have no will. One serious illness and the retirement corpus starts funding treatment rather than retirement.

Level 5: Self-Actualisation and Legacy

At the top sits what I call purpose-driven wealth: the use of money not just for security and accumulation, but for meaning. Charitable giving. Business succession. Building something that lasts beyond the individual.

Vikram eventually answered his own question. Once we addressed his Level 1-2 gaps and created a proper estate plan, the farmhouse project clarified too. It was not an investment. It was a plan to build a gathering space for his extended family – something he had been trying to recreate since his parents’ home in Mysore was sold. He was not missing money. He was missing meaning, and the inverted pyramid had been obscuring it.

Read: Medium Maximisation: Why More Money Is Not Making You Happier

Most financial plans are built upside down. Are yours?

RetireWise begins every engagement by checking whether the foundation is solid before optimising for the goals at the top.

Vikram had Rs 12 crore and felt like something was missing. The farmhouse was not the answer. The base of the pyramid was.

Build the foundation. Then build the rest. In that order.

Which level of the financial hierarchy are you building right now?

RetireWise works with senior executives to build complete financial plans – from the safety floor up to legacy and succession.

Your Turn

Look at the infographic above and ask yourself honestly: which level of the financial pyramid do you spend the most time and money on? And which level have you left incomplete? Share in the comments.

I am Not receiving followup posts/comments in my inbox….

Nice article

Hi Hemant,

Very good article really benifiting to look at the life of finance

Thanks a lot

Dear hemant sir,

very nice and useful post for us,pls guide us continuous.

thanks a lot

Hi, thanks 4 suggesting in financial matters through nice articles. i am 35 yr old working in a govt. project and not in permanent job, i want to know about any good pension plan, can you suggest?

Hello Hemant sir,

Very nice article.

Hi HEMANT,

Nice Article

Dear Hemant,

It is a very nice explanation of the part played by money in our lives. I wish to add one more point with your permission. Giving something back to the society from which we took a lot for our growth by way of charity. The immense happiness you derive by giving is something which can not be expressed in words. In my data sheet I always add this Charity item to create awareness. Thanks lot for a wonderful write up.

Hi Hemant

Nice way of putting financial matters for the benefit of many in a nice way.

one must learn to enjoy what he has, little or more.

one must try to figure out that even little things he owns in life can be source of immense pleasure and happiness.

but at same time one must continue to strive for betterment.

great piece of writing !!! enjoyed reading it, would include the “giving need” as a part of self-actualisation — the peace and satisfaction one gets by contributing to charity or to a single unknown child’s education / well-being is way beyond words . giving back to society, in whatever small measure possible, will make us feel happy from inside.

Hi Shreedhar,

Oops I missed such an important point.

Your analogy is brilliant! Young people should be very clear about what activity gives them true happiness and do their best to earn their living in that area. Not always possible but one must at least try. This is a basic need almost the purpose of life. Unhappiness in ones job will reflect in all other decisions incl. finance.

Beyond this the purpose of life doesn’t have much clarity to me. If each of my actions are driven by commonsense, civic sense, humility, courtesy and basic respect for fellows human beings I think I have justified my existence as a human being which is either a freakish act of nature or a divine act of god.

Owning money and wealth is a bit of an illusion. We need the right amount of money at the right state in life which requires careful planning. Nothing more, nothing less. A basic sense of contentment is crucial for intelligent and calm investing.

Hi Pattu,

Well said, it’s really important that one should persue what he enjoy. Your comment must be read by everyone.

Hi Hemant

Very nice article.

Thank anil – these days we keep waiting for you comments 🙂