Last Updated on April 23, 2026 by Hemant Beniwal

“Best” is a word for eulogies. For investments, the word you want is “suitable.”

Every year in January and February, the same question floods into my inbox: “Which is the best ELSS fund for this year?”

I have been answering this question for 25 years. And my answer has never changed: there is no best ELSS fund. There is only the fund that is appropriate for your specific situation, held for long enough that performance has time to develop.

The question itself reveals a misunderstanding of how equity works. Let me explain.

⚡ Quick Answer

ELSS (Equity Linked Saving Scheme) is an equity mutual fund with a 3-year lock-in that qualifies for tax deduction under Section 80C – up to Rs 1.5 lakh per year. It is generally the best instrument within the 80C basket because it combines tax saving with long-term equity returns. For fund selection: consistency over 10+ years matters more than last year’s return. Look at rolling 3-year returns, not point-to-point. Pick 1-2 funds from established fund houses with long track records. Start a SIP and do not change funds based on short-term performance. Note: under the new tax regime (default from FY2023-24), Section 80C deductions are not available – ELSS is only relevant if you are under the old regime.

First: Is ELSS Relevant for You Under the New Tax Regime?

This is the most important question before anything else. From FY2023-24, the new tax regime became the default regime for all taxpayers. Under the new regime, deductions under Section 80C – including ELSS – are not available.

If you have opted for the old regime (either because you have a home loan, HRA, or other significant deductions that make the old regime more beneficial), ELSS remains one of the most attractive instruments in the 80C basket. If you are under the new regime, ELSS has no tax advantage – though it remains a perfectly good equity fund that you can invest in for long-term wealth creation without the lock-in constraint of the old ELSS framework.

Check with your employer or CA which regime applies to you before investing specifically for the 80C benefit.

Why “Best ELSS” Is the Wrong Question

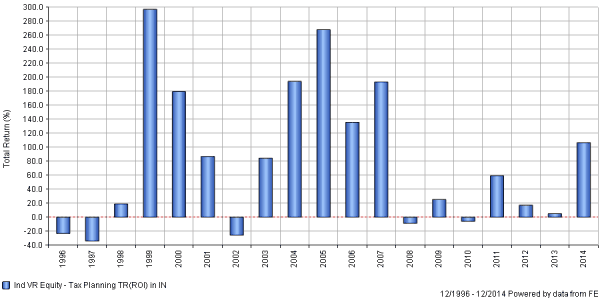

Consider this: if someone had invested Rs 10,000 in ELSS funds at the market peak in January 2008 (Sensex at 20,800) and withdrawn exactly 3 years later in January 2011 (Sensex at 19,100), some funds would have given negative returns. The “best” fund of 2006 or 2007 may have been the worst performer for someone who happened to invest at the peak and exit at the minimum lock-in.

The problem with selecting based on recent returns is survivorship bias and mean reversion. Funds that top the charts in any given year are often there partly because they concentrated in a sector or theme that happened to outperform. That concentration can become a liability in the next cycle.

The investors who made money in ELSS are not the ones who picked the “best” fund each year and switched. They are the ones who picked a reasonable fund from a reliable fund house, invested through SIP, and held through the lock-in and beyond.

ELSS selection is a 10-minute decision. The 10 years after is what matters.

RetireWise selects ELSS and other equity funds as part of a complete goal-linked investment plan – not as a standalone tax-saving exercise.

What Rolling Returns Tell You (That Point-to-Point Returns Don’t)

Point-to-point returns (e.g., “5-year return ending March 2024”) are heavily influenced by the starting and ending points. A fund that happened to be high at your measurement start and low at the end looks terrible – but may be perfectly good over most other 5-year periods.

Rolling returns eliminate this problem. A 3-year rolling return calculates the annualised return for every possible 3-year period – starting January 2010, February 2010, March 2010, and so on through to the present. This gives you a distribution of outcomes: how often has this fund delivered positive returns over 3-year periods? What was the worst 3-year period? What percentage of 3-year periods gave more than 12%?

Looking at the rolling return chart above: there are negative 3-year periods – all of them starting at or near bull market peaks. But as the holding period extends to 5 years, negative periods almost disappear. The lesson is not which fund had the best rolling returns – it is that time horizon matters more than fund selection.

How to Actually Choose an ELSS Fund

There is no magic formula, but there are sensible criteria. Look at fund houses with long track records and professional fund management – the AMC’s overall reputation and investment process matters more than any individual fund manager. Look at consistency: a fund that has delivered 12-14% CAGR across multiple market cycles is more trustworthy than one that delivered 25% in one year and 3% over 10 years.

Avoid concentration in a single fund. Spreading across 2 established ELSS funds from different fund houses reduces the risk of one fund manager’s bet going wrong. More than 2-3 ELSS funds creates unnecessary complexity without meaningful diversification benefit.

Most importantly: do not change your ELSS fund because it underperformed for 1-2 years. Fund performance is cyclical. The manager who avoided IT stocks in 2021-22 (and therefore underperformed) may be the same one who outperforms when IT corrects. Switching funds based on recent performance is the surest way to always be in yesterday’s winner and miss tomorrow’s.

ELSS vs Other 80C Options

For investors under the old regime comparing 80C instruments: ELSS is generally the best long-term wealth creator in the 80C basket. PPF gives tax-free returns but at around 7.1% (subject to periodic revision), which barely beats inflation over long periods. Tax-saving FDs are fully taxable on interest. Endowment and money-back plans from insurance companies typically return 4-5% – below inflation after tax.

ELSS has the shortest lock-in (3 years vs 15 for PPF, 5 for tax FD) and the highest long-term return potential. The trade-off is equity volatility – your portfolio value will fluctuate, especially in the first year or two.

The lock-in, which most investors resent, is actually a gift. It forces the holding period that equity needs to work. The investor who cannot sell during the March 2020 crash (because they are locked in) is exactly the investor who benefits most from the subsequent recovery.

Read: ELSS vs PPF: Which Is Better for Tax Saving?

Stop looking for the best ELSS fund. Pick a consistent fund from a reliable AMC, set up a SIP, and hold through the lock-in and beyond. The return you earn will be determined far more by how long you stay invested than which specific fund you chose.

Consistency beats selection. Time beats timing.

Are you investing in ELSS as part of a plan – or just to save tax?

RetireWise integrates tax planning with long-term investment planning – so every rupee of tax saving is also building toward your retirement corpus.

Your Turn

Are you under the old or new tax regime? And have you ever switched ELSS funds based on recent performance – and how did that work out? Share in the comments.

Sir,

I am an NRI, 42 years old, working in Muscat. I have been reading your web articles since 2011. Even though new to mutualfund investments, I used to watch your fund analysis carefully to compare fund performance and return.

I have started an NRE Recurring deposit A/c last year for Rs.10000 per month with 9.5% interest. I will get Rs.20 lacs approximately from this RD as maturity amount.

Now, I would like to make a mutualfund portfolio with Rs.12000 per month in SIPs with a tenure of 10 years. As I have already started investing in RD, I have selected 6 mutualfund schemes which are aggressive in nature but follows the value investing method. The schemes are : Birla SL Pure value fund, Canara Robeco Emerging Equities, Franklin India Smaller Companies, ICICI Pru Value Discovey, L&T India Value fund and ICICI Pru Exports and other services fund (Rs.2000 pm in each fund).

The above portfolio gives allocation in main sectors as follows : Finance-14%, Healthcare-13%, Technology-11%, Construction-10%, Engineering-8%, Chemicals-8%, Service-8%, Automobile-7%, Energy-6% and FMCG-3%.

I have included the ICICI Pru Exports and other services fund in this portfolio deliberately to give sectoral weightage in healthcare and technology. (Without this fund, the above portfolio will have an over-weight in financial sector and under-weight in healthcare sector). Is it a right allocation strategy.?

Also please note the stock characteristics of this portfolio : P/E Ratio-17.58, P/C Ratio-6.13, P/B Ratio-2.75 and average portfolio management fees will be 1.38% pa.

Can I go ahead with this plan.? I will be obliged if you could analyse and share your expertise to fine tune my selection. Please help.

I have been invested since couple of years in ELSS & other mutual funds through SIP mode. I have at present investment in Axis Long Term Equity – Direct (G) 2000 rs/month, Reliance Tax saver – Direct (G) 1000 rs/month. Also investing in SBI emerging fund (G) 1000 rs/month & UTI opportunity fund (G) 1000 rs/month. Till date I am getting positive return considering all funds accumulation.

I want to invest another 3000 rs/month in ELSS funds to get tax benefits along with higher return then conventional tax benefit investment options. All present & new investment are for long term investment horizon and I am open for low to medium risk fund houses.

Can you suggest where should I invest for 10 + years of investment horizon.

I think that one should select the best elss for him on the basis of his investment time horizon, risk profiling and acceptance level for volatility. Past numbers are useless.

If I want to invest in a lower risk scheme then elss with large cap bias with low beta is suitable and if I want to invest in high risk high volatility scheme, obviously either a tactical call or long term investor or long term sip investor, then one can think for funds with small and midcap bias.

Hemant jee, can you please carogarise the elss schemes wrt risk and rewards?

Hello Sir,

I am new in mutual fund investment. Need support.

I am looking to invest in ELSS.

Can you please suggest me best 3 or 4 ELSS funds to invest based on current market performance or situation ?

As per my analysis, Axis long term equity & Franklin India Tax shield are good one.

I saw top 10 performing, but confused which one to select.

Hopping for quick support.

Thanks.

What is the difference between investing in MF directly and through an agent. What difference does it make in servicing and in terms of returns.

Dear sir,

I have go through with your Post,

i am planing to buy a term plan to secure my family. request to help me buy a best term plan for me.

I am 31 year old and income is 6L/A, depend are my wife only hope after few yr a kid also.

i am smoker a day 3-4 max and light drinker in month only.

i am confused with LIC, HDFC and ICICI, i want to buy a term plan which accidental death also.

please help for 50 lacs cover

Thanks

Kripa

Burnt my fingers in Sundaram Tax Saver, which at the time of investing, was the top-ranked fund. Staying away from ELSS now.

mr. kc , i advice u for axis long term equity. in last 5 yrs. it the best performer in this group.keep patience because your money is gonging through sip in equity. wait for long term.

Hello Hemant,

I would like to know if i can invest a certain amount in elss through sip mode for 7 years and whether i can get tax benefit for 7 years in 80C?

Dear Rohit,

Yes you can invest & get tax benefit every year.

Dear sir, I have been investing through sip in hdfc long term advantage fund growth since Aug 2012 then to same scheme direct option from Jan 2013. Scheme was rated 2nd by crisil during period of Aug 2012 & now it’s rank 5. Should I switch it to axis long term equity or continue same. I want to invest for long term may be more than 10 yrs.When should v change to other scheme.

Kindly reply.

Thanxs.

Dear sir, I have been investing through sip in hdfc long term advantage fund growth since Aug 2012 then to same scheme direct option from Jan 2013. Scheme was rated 2nd by crisil during period of Aug 2012 & now it’s rank 5. Should I switch it to axis long term equty

hi,

good post . i am investing in quantum tax saver . what are your views on it.

A fund is good if it does better than average in the bull run (2009, 2013), does very good in the bear market (2008,2011).

My go to ELSS funds are Franklin Taxshield and Axis Long Term Equity