Last Updated on April 4, 2026 by teamtfl

In 2010, a client came to our office with a pamphlet. It said his Rs. 1 lakh would become Rs. 3.45 lakh in 8 years. LIC had guaranteed it, the agent told him. We told him not to invest. He did anyway — because his brother-in-law was the agent.

Eight years later, his Rs. 1 lakh had become Rs. 1.44 lakh. A return of 6.27% compounded annually. The Sensex in those same 8 years had gone from 16,000 to 38,000 — a return of 137%.

He was not foolish. He was trusting. And a system designed to extract commissions used that trust against him.

This is the complete story of LIC Wealth Plus — why it was sold, what it actually was, and what it teaches about insurance mis-selling that is still happening in India today.

⚡ The Verdict — What LIC Wealth Plus Actually Delivered

LIC Wealth Plus (Table 801) was launched February 9, 2010 and matured in 2018 after its 8-year term. Final NAV: approximately Rs. 14.44 — a return of 6.27% per annum since launch. Agents had promised 17–18% returns. The Sensex delivered 137% absolute returns in the same period (16,000 to 38,000). By 2024, the Sensex had crossed 85,000 — over 400% from the launch date. This product is now matured and closed. The lesson it leaves is permanent.

The Setup: How the Mis-Selling Began

Every year in the last quarter of the financial year, insurance agents across India face targets. In 2007, LIC launched a policy called “Money Plus.” Agents distributed pamphlets claiming Rs. 1 lakh invested for 3 years would become Rs. 3.38 crore after 20 years — at an implied return of 25% per annum.

People did not just invest their savings. Smaller households sold jewellery. Others borrowed money. The pamphlets spread across India — from villages in Bihar to offices in Mumbai. All promising returns “guaranteed by LIC.”

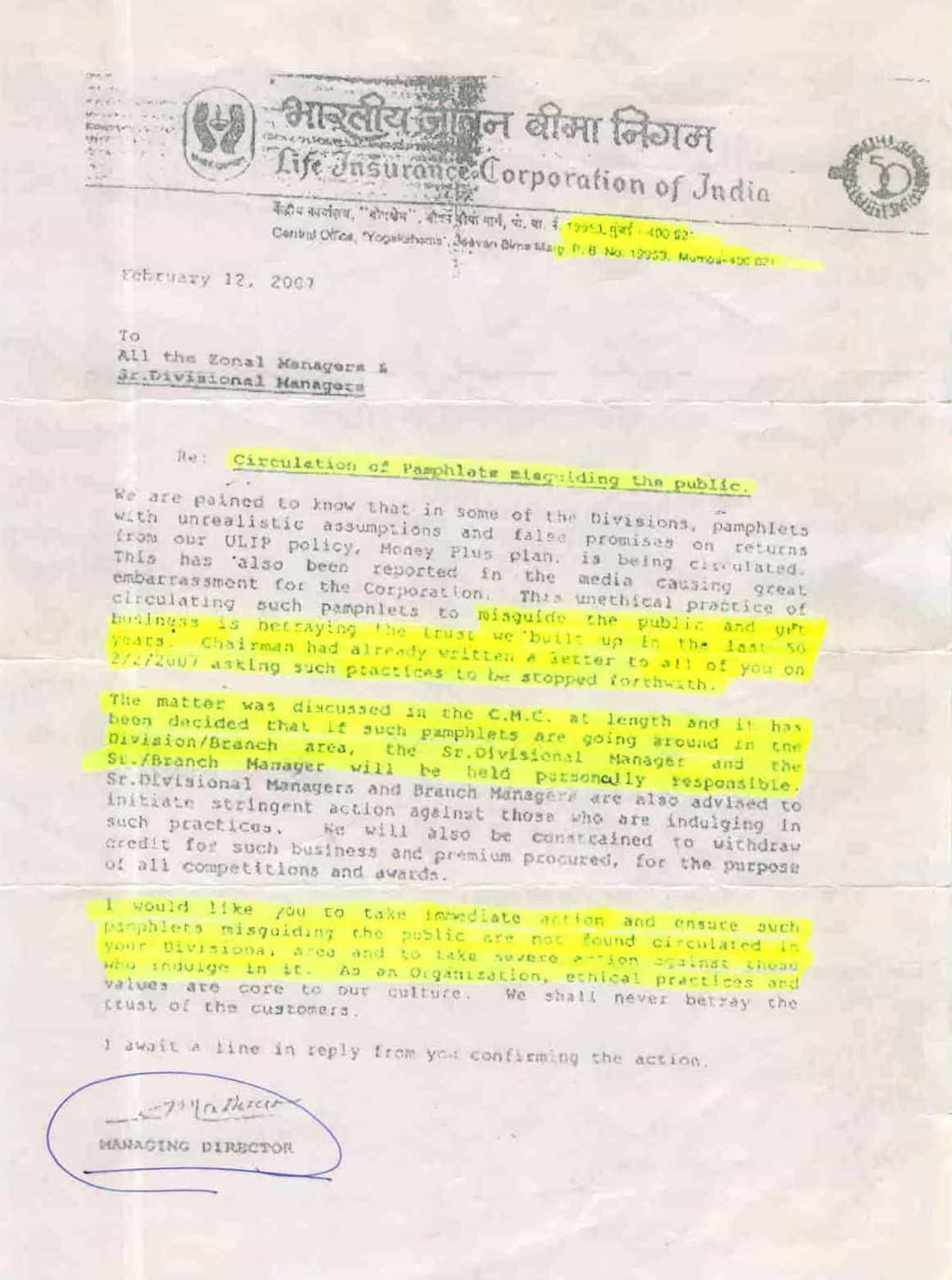

LIC’s own Managing Director, Mr. Mathur, saw what was happening. On February 12, 2007, he wrote to all Zonal Managers:

The letter called out “unethical practice of circulating such pamphlets to misguide the public.” The MD of LIC himself acknowledged the betrayal. And yet, three years later, LIC launched Wealth Plus — and the same cycle began again.

What LIC Wealth Plus Actually Was

LIC Wealth Plus (Table 801) was a ULIP — a Unit Linked Insurance Plan — launched February 9, 2010. Here is what the product actually said in its official documentation:

LIC would guarantee the highest NAV recorded in the first 7 years, with the product maturing after 8 years. There was a minimum NAV guarantee of Rs. 10 (the starting NAV). That is all. No return guarantee. No equity allocation guarantee. No promise of 17% returns.

In almost all ULIPs, the allocation to equity vs debt is clearly stated. Wealth Plus was deliberately silent on this. The fund manager had full discretion — which meant the money could stay largely in debt instruments, generating endowment-like returns of 6–7%, while agents told investors they would get equity-like returns of 17–18%.

What Agents Were Actually Telling Investors

The gap between what the product said and what agents told investors was extraordinary. Here is what agents were claiming:

That LIC was guaranteeing the highest return (LIC said highest NAV — a critical difference). That based on the performance of LIC’s earlier ULIP Bima Gold, investors would get 17–18% per annum. That Rs. 1 lakh invested would become Rs. 3.45 lakh in 8 years. That they should switch existing policies into Wealth Plus immediately.

The Bima Gold comparison was particularly cynical. That ULIP was launched in 2001 when the Sensex was at 3,000 — and ran through one of the greatest bull markets India had seen, with the Sensex reaching 21,000. Using that bull-market return to promise future performance was not just misleading — it was a manipulation of trust.

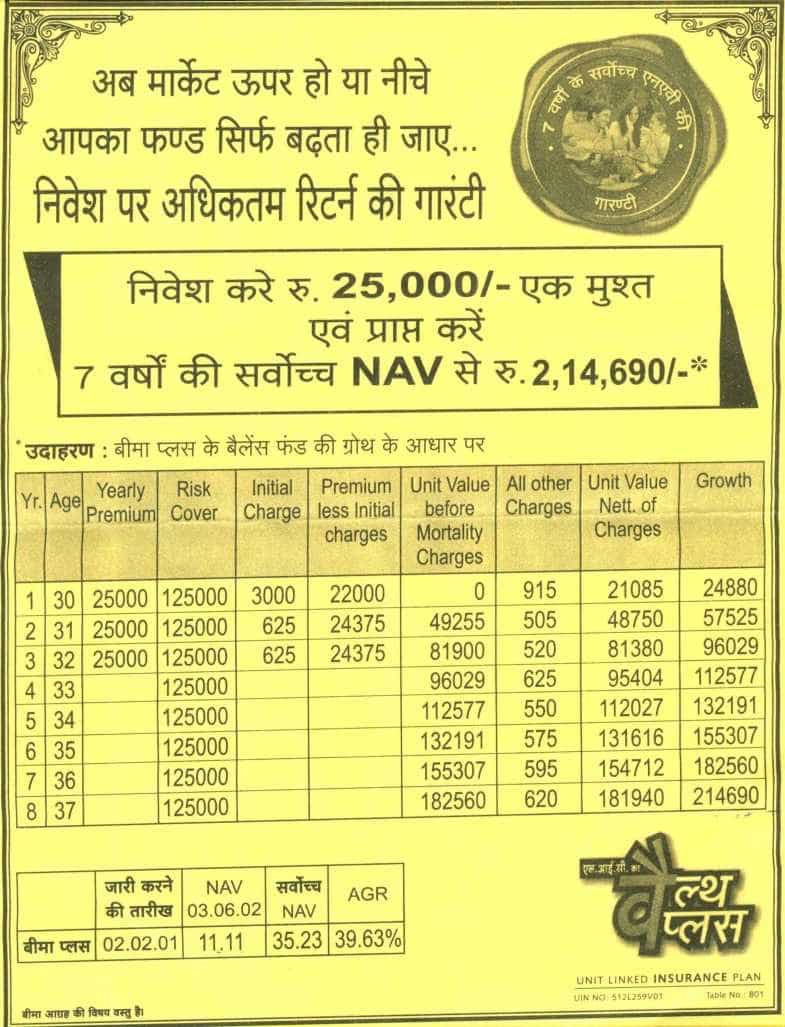

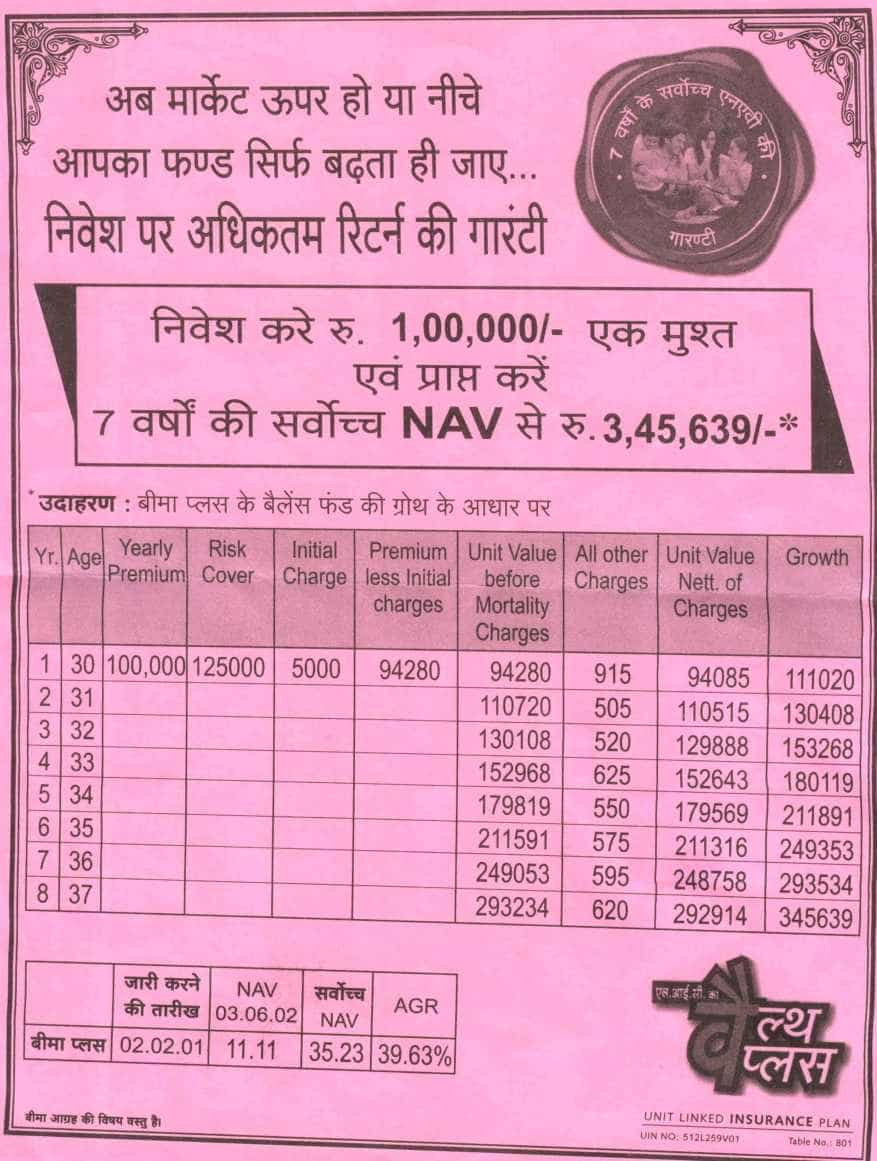

Below are the actual pamphlets distributed across India:

Pamphlet: Regular Premium — Rs. 25,000 for 3 years

Pamphlet: Single Premium — Rs. 1,00,000

What the Regulator Said — and What Actually Happened

IRDAI (then called IRDA) mandated that agents show returns at only 6% or 10% in official illustrations. No pamphlet had any regard for this. The gap between what agents promised and what the regulation required tells you everything:

| Regular Premium (Rs. 25,000 × 3 yrs) | Single Premium (Rs. 1,00,000) | |

|---|---|---|

| Pamphlet promise | Rs. 2,14,690 | Rs. 3,45,639 |

| IRDA projection at 6% | Rs. 87,549 | Rs. 1,18,442 |

| IRDA projection at 10% | Rs. 1,14,306 | Rs. 1,61,697 |

| Actual NAV at maturity (2018) | ~Rs. 14.44 (6.27% CAGR) | ~Rs. 1,44,000 (6.27% CAGR) |

The product landed almost exactly at the IRDA’s 6% illustration — the lowest scenario regulators mandate. The agents had promised 17–18%. The reality: 6.27%. Not a slight underperformance. A systematic betrayal of trust.

💡 As D. Swaroop (PFRDA Chairman at the time) stated on record: the chief cause of mis-selling is the incentive structure that induces agents to look after their own interests rather than those of the customer. The average sum assured of the insured Indian was less than Rs. 90,000 — because agents sold investment products, not insurance. That problem has not disappeared.

Holding insurance products you don’t fully understand?

At RetireWise, we conduct annual portfolio audits to identify underperforming products — ULIPs, endowment plans, and money-back policies that are quietly dragging your retirement corpus down.

Why This Keeps Happening — The Incentive Problem

The agent who sold LIC Wealth Plus was not necessarily evil. He was responding rationally to a commission structure that rewarded selling over advising.

High-commission products — ULIPs, endowment plans, money-back policies — pay agents 25–40% of the first year’s premium. A term plan, which gives the customer far more insurance cover for far less money, pays almost nothing. So agents sell what pays them, not what protects the customer.

Insurance agents in India have sold to Indians everything other than insurance.

The solution is structural: work with an advisor who earns a fee from you, not a commission from the product. A SEBI-registered RIA has no incentive to sell you any product — their only income is your advisory fee. That changes everything. For a full guide on what to look for in insurance and what to avoid, read our post on 9 insurance questions every Indian gets wrong.

The Lesson That Does Not Go Stale

LIC Wealth Plus has matured. The product is gone. But the lesson is permanent.

Every quarter-end in India, agents still face targets. Endowment plans are still sold as “safe investments.” Guaranteed return products still promise returns that are not guaranteed. The pitch has evolved — it is digital now, it comes on WhatsApp — but the structure is identical.

Before accepting any financial product: ask the agent to show you the IRDAI-mandated illustration at 6% and at 10%. That is the worst and moderate scenario. Make your decision based on those numbers, not the pamphlet. If the product does not make sense at 6%, it does not make sense.

And if you are currently holding a ULIP, endowment plan, or money-back policy that has been running for more than 5 years — get the IRR calculated. The true internal rate of return on most such policies is between 4% and 7%. Your EPF earns 8.15%. A simple index fund earns 12–15% over the long term. This is the comparison that matters. For how to audit your portfolio and exit products that are working against you, read our post on 9 smart ways to save money in India — specifically the annual portfolio audit section.

The man who came to our office in 2010 with that pamphlet was not foolish. He was human. He trusted a relationship. He trusted an institution. Both let him down.

The best way to honour that trust now is to never let it happen again — to you or anyone you care about.

💬 Your Turn

Did you or someone you know invest in LIC Wealth Plus in 2010? How did the final returns compare to what was promised? Share below — your experience helps others recognise the same pattern today.

Yes it is complete cheating. Innocent public are taken for ride. In spite of extremely very low return, they deducted a TDS of 1% of maturity money, and declared to IT dept that the total maturity money is my income for this year. That meansi i have to pay 30% of my maturity value as tax. Mismanagement of weath plus fund totally, and with a defectful clause in terms of tax on the maturity. Some one has to take up this seriously.

Hello,

I think the whole purpose of this Policy is Death Cover i.e. 50 L at the most.

Disputed Points:

1. Accident Cover is between 50,000 – 50,00,000/-

2. The policy is for 8 years + 2 years extended.

3. Accident Cover cannot be claimed in an extended period.

4. The policy starts with 10 FAV i.e. the time one has invested he/she is in negative on the first day.

5. The policyholder is entitled to get the report of NAV every year.

Solution: One can file a case in consumer forum taking appropriate grounds.

Thanks a ton to Mr. Hemant Beniwal for posting Circular of LIC.

Nishant Patil

(Advocate, Bombay High Court)

[email protected]

Its cheating LIC doing.. I just received rs 43200 for rs 40,000 invested in 2010. Its gross misappropriation of funds and LIC should reimburse. I think we all should make a group and file a case against LIC. Also thrash some LIC agents who come to you with any stupid plans and thrash some LIC ppl. then they will know for sure what they are doing.

Hi Hemant,

Can you please advise me as to where to find my total number of units in my lic page. Cant find it 🙁

Also how to redeem policy money back without visiting LIC office. Is there any form which can be filled online where we provide the bank details?

Thanks,

Kritika

Hi Kritika,

Talk to any LIC agent in your area – he may help you.

Hi Hemant,

Where to check number of units in my account? I checked online for my wealth plus policy, but not sure where to find that in site on my lic page. Need your urgent help. As already late in retrieving my money 🙁

Can we fill some online form for redeeming policy money by giving account number?

Please help with the info. Thanks in advance!

Kritika

i have invested rs. 7 lakh in wealth plus over a period of three years during 2010, 2011 and 2012, LIC is paying me only Rs. 764000/- due to agents and premium collectors.

I shall not advise anybody to invest in LIC because of the experience.

Sorry to hear this Dr MK Gajera

Sir I invested 12500×6=150000 in 8-05-2010 to 8-5-2011 after maturity2-7-2018 LIC gave me only 110000 why less money gave me. Policy no. 236794617

Ask your agent.. Give him nice thrashing and also the LIC ppl.

Dear Sir,

I have cheated by LIC I have invested RS 50000/- in wealth plus table no 108, my agents said that in 8 year LIC will give you highest NAV.but after 8 year you can’t imagine what l got from LIC that is RS 64000/- only.I highly recommend that don’t invest in LIC, it is better to invest our money in bank,Post Office,and private coy like Baja alliance ect because pvt coy gave better return than LIC,LIC is very bakwas coy don’t trust it.

Big Cheating !!!! Cheating !!! Cheating!!! Is there any group where we can file a case against LIC ??? i invested my hard earned money 40k in 3 policy in 2010 and after 8 years what i am getting now is 46k ….. i will never trust on LIC any more .. LIC is Big cheater .. We all should unite and take action against LIC

Reply

Kindly advise tax treatment on the Maturity, Will Indexation shall be applicable to calculate CAPITAL LOSS?

LIC has cheated me by their policy Wealth Plus. Bcoz LIC agent told me that if i pay Rs. 40,000/- once for purchasing wealth plus policy, after 8 years i will get minimum Rs. 1,50,000/-. Hence, i had purchased wealth plus policy for Rs. 40000/-

Now the policy has expired and when i submitted to LIC office , i only got Rs. 52,000/-.

So i request everyone to check & think twice before purchasing any LIC policy.

U R LUCK I GOT ONLY 49105

I invest 50000 in march 2010 in lic wealth plus

can you please tell me how much amount i will get in the end of march-2018

please reply

Dear All,

LIC is really Bull Shit.

My Parents invested their Hard working Money 1 Lacs Rs in LIC’s Welth Plus Policy in year March 2010.

In April 2018 after 8 Years they received 1 Lacs 4 thousand Rs.

this is really Joke by LIC, they really Cheating with their Loyal customers.

I feel very Angry and helpless for my parents and can not do anything now.

BEWARE FROM SUCH FALSE COMMITMENTS FROM LIC

AT LEAST SUCH TYPE OF CHEATING NOT EXPECTED FROM LIC

HOW PITTY, JUST TO GAIN SOME PROFIT LIC OF INDIA BEHAVED WORST THAN LIKE LIC OF PAKISTAN. WHILE ASKING MY AGENT, HE TOLD AT THAT TIME MANAGERS GUIDED 3 -3.5 TIMES OF INVESTED AMOUNT WILL BE THE MATURED AMOUNT. WE COMPLAINED. DON’T KNOW HOW MUCH FACT IS IT. LIC LOST ITS CREDIBILITY AS WELL AS THE AGENTS TOO , AGENTS ARE ALWAYS AGENT THEY WILL NEVER BE MORE THAN THAT.

This is with referance to your artical, about LIC agent and tag line AAP KI YAA AAP KE AGENT KI

This refers to whole community of Insurance advisory.

Before writing this article Do you know ?

1. What is the standard division of this product.

2. what Is mean ?

3. What is HPR

Is that anything declare by any Insurance company or any Mutual fund company that what will be Future value of the equity base product?

there are so many mutual fund and ULIP product, they had performed below benchmark returns.

so understand everything before writing wrong comment to any professional community.

Hi Jignesh,

I understand all these points that you have mentioned & you will be surprised I have written 2 posts on these topics. Not sure how you are justifying mis-selling of this product.

ALL LIC agents are cheaters…saale logo ka paisa kha gye cheaters

Typo: Reach => Rich (Admin please)

LIC is good for reach people. Your principal will be safe for sure.. Most of the our hard earned money are taken by the agents. My wealth plus investment of 1 lakh after 8 years is just 1,34,000 on feb 2018. A saving account is far respectable. LIC sucks. I will make sure that my children never opt for LIC. Had my father lived today, he would repent for the decision he made for us for our future. And mostly in India business based on lie. If not, why LIC does not place strict rules for the agents(trained shameless lairs?) so that the customers are not duped. It is not always possible to read and understand everything between the lines. People invests in faith.

I purchased wealth plus with rs 100000 single premium in 2010. After 8 years I sent for redemption. I was shocked when I received just rs 105853. When I contacted LIC they told that I was lucky to get 5853 profit after 8 years because my age at entry was 57.

lic welth policy is fraud policy .it represted by lic officer to earn for own not for policy holder . they are at the of paid premiem invest one lach you get 4 lakh after 8 year. but they gave only 1.35 lakh.this is fasvnuk policy .agent and lic officer is also froad .only collect the from the genral poor public. only show high return but not given

I Urmila Ashish Bansal taken policy of Wealth plus on recommendation of agent mr Jayprakash of Rs. 40000/-after waiting for 8 years i.e on maturity i received Rs.39861/-its a bonus they have given principle amt has been eaten upby LIC i feel cheated by LIC and its shear nonsense on their part. begining they were claiming amount would get doubled but this way bank also does not do.POLICY should be”” Wealth minus””

I Urmila Ashish Bansal taken policy of Wealth plus on recommendation of mr Jayprakash of Rs. 40000/-after waiting for 8 years i.e on maturity i received Rs.39861/-its a bonus they have given principle amt has been eaten upby LIC i feel cheated by LIC and its shear nonsense on their part. begining they were claiming amount would get doubled but this way bank also does not do.POLICY should be”” Wealth minus””

very ashmed to write here that LIC cheated they have taken Rs.100000/- in 2010 wealth plus and

after 8 years they paid Rs.132491 after deducting tds 1325/- means we are assuming it will be Rs2lacs and above, but this is shameful, those LIC agents and ULIP holders mangers should see the jail , I want to make a court case against this cheating with LIC India Pls suggest any good advocate or legal action against LIC so that in near future they should not loot the general public with bloody dog agents, Today I have decided that if any LIC agent will approach to me I will shoot only gaaali and he will not get any respect from my side.

Agree There was no clear picture of the policy even I faced the same issue. Do we all have solution on this .

The money of Wealth Plus was invested in the company of Kirti Chidambaram during the Congress government period. Now, during the BJP government, some scams of Kirti Chidambaram came out, among them LIC is a scam. But it did not disclose as LIC should not cause damage. That company met less of the closure of the shutdown … make sure …

Mahesh ji Maine bhi 40000/- same invest Kiya tha 26/3/2010 aur ab 31/3/2018 ko LIC me cheque Diya h 52469/- Ka aur aapko keval 44023 Ka ,ye company to sabhi k Saath cheat Kar rhi h

I paid Rs.20000 for 3 years ( wealth plus) =Rs. 60000 on 20/03/2010 , Policy no 498134074

Please send me policy status ( NAV units, NAV) or Maturity Value

My policy no 498134074

Please send my policy status (NAV units,NAV)

I Have Paid Rs 20000 per year x 3 year = Total Rs 60,000 in 2010-2011.

Now I got 75,992/- ( after 7-8 year i.e. 26% return in 7-8 year, i.e. 4% return in the year which is less than saving acount ).

I feel that LIC has made Joke.

Yes Ashvin. Even I got the similar amount. LIC has cheated in this case. They have wrong promise. They should be sued in the consumer court which I am planning to

I Have Paid Rs 20000 per year x 3 year = Total Rs 60,000 in 2010-2011.

I got now 59112 rupees only…..

I feel that LIC has made Joke…

I Have Paid Rs 20000 per year x 3 year = Total Rs 60,000 in 2010-2011.

Now I got 75,992/- ( after 7-8 year ).

It is like Joke by LIC.

I invest 50000 in march 2010 in lic wealth plus

can you please tell me how much amount i will get in the end of march-2018

please reply

Hi, My policy just got matured on March 31, 2018.

These are the details:

Investment year: 2010

Investment amount: Rs 60000 (paid in three years).

NAV Units (as on April 3, 2018): 5219.

NAV: 15.5725

The assured sum is 1 lakh.

Can you please calculate for me how much will be my earnings. Thanks

I have purchased LicWealth Plus on26.3.10 for rs.40000.And on maturity I have received rs.44023.00 only on 31.03.2018.Is it wealth plus or wealth mines?LIC should reply

I read your article and You are right I was cheated too. I invested 20000 annually for 3 years in wealth plus. My maturity was on the 10 of march 2018. When I went to the branch and asked the officers what will be the maturity value they did not cooperate . “You will see when you get it.” was their reply. yesterday Rs. 79550 was credited from LIC. I invested 60000 and and got back 79000 after 8 years. This is gross bull shit, what kind of stupid policy is this? Can you please explain how and at what percentage the return was calculated?

lic chor sale 50000 inwest kre welth plus me or 8 sal bad mile 66000

Dear Sir,

just matured my walth plus policy no 959234056 after paying 30000 annually for 3 yrs from 12 march 2010.

i just got on 17 march 2018 maturity amount 121856only. is it correct as per your calculation. or what to do with LIC, pl guide

I have cheated by LIC. I have invested 3,00,000.00 in wealth plus plan my agents said that in 8 year LIC will give me 9,44,000 Rupees all time highest NAV, but after 8 year you can’t imagine what I got from LIC 4,17,940 only. I highly recommend that don’t invest in LIC and don’t trust any LIC agents.

MY Policy no is 428436372.pls send my policy Status.(No of unit & Nav valu)

Investment of 300000 lacs after 8years I got 417900 lacs I feel cheated. Does anyone help me.

Lic wealth plus policy is only for their mutual ( LIC , LIC Agent’s & Govt. Of india ) benefit , it is not for policy holders benefits , mostly LIC & LIC Agent’s are cheated of their customers.

I was also invested 40k in single premium & got only 50998 on maturity.

CHEATING PEOPLE IS LIC’S POLICY

sir its a hopeless policy where everyone has been cheated.I have invested 3 lakhs for my daughter’s marraige where i was completely disappointed u people have cheated everyone i really feel like putting up this msg on social media face book twitter everywhere and show your lic real face .

Hello Hemant,

I have invested approximately 72,000/- in LIC Wealth Plus in three years which ended into 2013. How much NAV unit I should have and what maximum return I will have after 8 years of investment. Can you please help me to understand this. I hope in Mar’18 maturity benefits are there for me.

Dear sir

I had invested One lac single premium in Wealth plus in 2010. Please tell me how much I will get in March 2018 that is date of maturity.

Hope you will reply

not more that 125000 they cheated all of us.

my policy matured 2 days back i invested 50000 one time premium and got only 61000 they are fooling us.

and after arguing with manager he said you got some profits even their are some people who got less than invested money.

I have invested in Lic wealth plus…feeling disappointed with returns so far….

The LIC fund manager is responsible for the poor performance and cheated with the Trust of lic investors, those being invested in fund for 8 yrs in hope that in rising market fund will perform at par with the mkt….Feeling cheated and LIC should think seriously about thr solid investors Trust and not reviewing the fund performance time to time like thr big hdgs at the time of launch !!

sir

i invest lic wealth plus rs. 75000 year 2010. as lic mentioned highest nav they will return. but current nav 15.52.

period from 2010 to 2018 what is the highest nav for lic wealth plus scheme

I invested 20000 in 2010, 20000 in 2011 and 20000 in 2012. (3 yrs paid) in wealth plus. after that waited for nav to grow. if i surrender now how much will i get ?

Sir, I have started the wealth plus policy by 40000 on 20-03-2010 at present how many money i get…

Respected sir I was invested 100000 rs since the started the policy what is the current value of money

Lic is making fool to all innocent people of India.

Sir

I have invested Rs 50000 single premium in LIC wealth Plus in April 2010. What would be the value of the investment as on today?

NOW IT IS LICC- LIFE INSURANCE CHEATING CORPORATION

I HAVE INVESTED RS,65000/- IN EQUAL MONTHLY INSTALMENTS FOR 13 MONTHS. I HAVE NOT PAID THE BALANCE PREMIUM FOR NEXT 23 MONTHS. HOW MUCH MONEY I AM GOING TO GET. PL REPLY

I never imagined that LIC can be a master of cheaters. I invested 120000 in wealth plus and got 125000 only after 7 years. What a joke?. I can never recomend LIC to any body.

Earlier the same thing happened with master plus. I had to take money back after 3 yrs.

LIC is the biggest fraud company of India. It has cheated mainly Middle class and poor people of our country. But all our Governments including the current of Mr. Modi, has given licence to cheat and loot the people of India. Not only that, this is nothing bit a corruption. If you collect crores of rupees from people on false promises under full knowledge of Higher Management and Top Official and Ministers of Government, How can you you say that, we are not responsible and only people who has taken policy are responsible. Because Government whenever wants money for disinvestment, they force LIC, at the cost of People. Look at any policy of LIC, have you ever got return above 6 %. At least I have not got. I have maximum exposure to LIC. I am ashamed. What can be done. That is why we say , India is Great.

all the lnsurance company are giving only 4 to 5.5℅ pa avg. IRDA was unknown .now they are wakeup but now investors are going to sleep

Yes Krishna – in traditional plans we can’t expect more than this. ULIPs are anyway related to markets.

The best way to remedy the fiasco of Wealth plus plan’s investment and lowest returns is to waive the entire Allocation charges and Admn. charges levied so far by LIC and settle the Fund Value along with the waived charges to investors on the maturity date.

Hi Jayakumar,

This is wishful thinking – LIC or any other product manufacturer will never do it.

shame on lic and there agents. they play game for his benefit from hardearn money from investors like me. my family hope collapse due 2 this policy. TRUST ON LIC IS REDUSED . I CONSIDER ON MY ANOTHER LIC POLICY TO BE CONTINUED OR NOT.

Sir, I have started the policy by on200000 28-03-2010 at present how many money i get…

Sir, I have started the policy by 200000 on 28-03-2010 at present how many money i get…

Sir, I have started the policy by 200000 on 20-03-2010 at present how many money i get…

Sir,

My Policy No. is 494504783. Paid @Rs. 50000 for three years. 7th year completed.

Please inform about the amount of fund / surrendered value now.

Regards.

Note we cannot clap with one hands. Similarly LIC and agents are working hand in gloves to fool customers and the blame is pushed on agents alone. If you are aggrieved by agent not giving service and wish to change agent , LIC will straight away not cooperate you and that agent will appear life long in the policy. If agent is not giving service for non earning and you ask LIC the amount of commission paid in your policy , LIC will reply that you( the customer ) is a third party in his own policy and hence LIC cannot share information. Lic is working hand in gloves with agents to fool customers.

LIC think that they are above law and dictate their own terms. Each branch has its own decisions in issuing a policy though it is a central act. I have vey bad experience with LIC and hence forth I will never invest any money with lic. I gave tough fight to LIC in rti and thus saved my one policy and saved my 1,75,000 rupees. I gave another chance to LIC again they cheated and closed my 6 polices only because I threatened to go to court. I somehow again under rti revived my polices but LIC extorted money from me and the matter is in court own for refund of excess premium. All those who are reading this please note lic high level officers as well as senior agents are not aware of many facts or they are fooling customers. Recently LIC published PM Modijis photo in their pension plan. In pension plan there is no insurance still signature is taken on section 45 of insurance act which should never be signed in pension plan . The senior Crm have admitted their mistakes orally but still have failed to remove the same from the form of pension plans. Please friends do not sign blindly on insurance forms . While filling forms be very cautious regarding your health. Even if your health is good write I don’t know I don’t remember and insist LIC to do medical otherwise they have very good reason to reject claim. Somebody mistake or weak point is taken as opportunity by insurance companies to fulfill some another claims and also to earn profits. LIC has harts passed me from pillar to post and they are white collar criminals. But LIC don’t know that people are not educatednow .There is technology.

,rti,consumer protection act etc.mi have read thousands of judgements of ombudsman maximum are in favor of LIC . Consumer protection act though a consumer may succeed at district or state level but very less people succeed at national level. Consumers have only 15 days to cancel policy but insurance companies have two years and now it appears that same has increased. Also LIC does not provide copy proposal form to its customers . Also as per terms and conditions of LIC , LIC is not bound to give reminders for renewal of premium and In that case agents do it apprroach and consumers forget ,lots of hardship is caused to consumers. Thus my request is to invest very small amount which even one can forget and if one wants to really put big money consult a good consumer lawyer who is well versed with insurance policies and the

Invest money.

Sir I have by lic wealth plus in April 2010 and paid 40000/year for 3year and paid all three primium total 120000 and my policy matured in April 2018 how many return I got sir

i have invested in wealth plus, i got wrong feed back from agent, and also blindly trusting lic, but today my fund value is notthing, fund mangement are more knowledgeble, but today I am looser , my investment is Rs.200000/ who is responsible ? for misguiding us, if we are making any single mistake, then same lic is ready to punish us with high penalty, now who will solve my problem

Sir

I invested wealth plus Rs 40,000 one premium on 13.04.2010 Sir what is the highest NAV so far it attained Kindly let me know

14.65 is the max till now i have invested 3lac now after 8 years getting 3.8lac only how sham on lic bloddy bugger agents

dear sir, many thanks for your article. but according to me whatever may be the reason, we have done this policy. now what should we do? will sell it at present NAV or hold it because as per my knowledge LIC may go for a IPO and it happens then certainly NAV will go up beyond our expectations.

I am also cheated by LIC agent by selling LIC Market plus (wealth plus) plan 801 with single premium Rs 100000.00 on 22.03.2010 maturing on 22.03.2018 further extended 2 yrs to 23.03.2020 and misleading me giving wrong information. Please give me best advice what should I do? 12.07.2016

Sir, i took one policy of lic wealthplus plan no. 801 in 2010.now i want to know my policy status .can you send on my email id.

LIC WELTHPLUS is a robbing scheme they have cheated public royally, they are great Mismanagers that’s why they are working for LIC apart from wrongly investing they are also charging Admin charges for the bad work being done by them. I will never invest in LIC market linked schemes.

sir my wealth plus L I C policy three year premium amount 20000.00 per year start policy month/ year 20/4/2010 date of expiry of the policy 20/4/2018 want to surrender my policy/ partial withdraw can I know what amount will return my policy no 766505761

I invested Rs 95000/= in LIC wealth type in March 2010. My agent advised me to surrender this policy in Nov 2014. The surrender value was just Rs 1,03,237/= i.e hardly 5% gain over a period of 4 years and 8 months. Further TDS @25 was deducted on the total fund value i.e.Rs 1,03,237/= . With deduction of TDS, I need to include the entire fund value in my taxable income for the FY 2014-15. That means I need to pay Income tax @20% on the entire fund vaue of Rs 1,03,237/= . Thus the amount I receive after paying IT @20 % would become less than Rs 85000/= That means against investment of Rs 95000/= , I am receiving an amount of Rs 85000/= after 4 years 8 months. LIC and its agents are great. I did not expect such a cheating from a reputed Govt of India Company , LIC. Can we believe our Govt to help small investors against such cheating.

I have invested Rs. 1 Lac in year 2010 in Wealth plus. I would like toknow how to check NAV so that whenever there is little hight that return little more than lac I can surrender the policy. But want to know the calculation and what the no. of units.

DEAR SIR

I am invested 2LACK -N 2010

PLEASE INFORM WAHT IS MARKET VALVE TODAY DATE l

PLZ HELP AND GUIDE

i have invested Rs. 100000.00 in wealth plus 801 on 20.03.2010..

as on date bse sensex is approx 67 percent up..

if i keep ma money in debt/FDR in 4 full year.. i assume ma money wud have been atleast 40 percent up..

where the fund manager have invested the money i don know.. as on date my NAV is 11.89 only .. its means only 19 percent up..

i wanna ask fundmanger where they have invested ma hard earning.. surely not in stock market.. not in debt..

plz help and guide me can i sue fund manager for dis.. i m feeling cheated by heart..

plz help me

I invested Rs. 50,000/- in LIC Wealth Plus in Feb. 2010.

Since I’m in need of cash, what is the net amount I shall get upon surrender of the policy .

I have took wealth plus in 2010.I have invested 20000 each for three years trusting the LIC. Please suggest shall i took the money or keep it for another 3 more years ( total 7years).

Please suggest

hi sir…., can it is possible to file a case in consumer court against the LIC for this cheated policy? plz give me answer as possible…………thanks

Respected Sir,

I have by chance come accross your site and believe me your explanations are wonderful as I am also one of the foolish/layman investor who wanted to become rich in a short period. Can you kindly sujjest me some place where I can invest money and get a return of 12%. My top priority is safety as I am a salaried person and if I loose money now I may not be able to earn it again. My age is 48 yrs.

Thanks

Best Regards

Amit Moitra

9818500000In view of the above commenst of the investors, what is the opinion of LIC regarding wealth plus plan as the NAV of wealth plus plan is down is compare to the sensex

I have received the unit/NAV statement from LIC for the current year for the wealth plus 2010.I have invested 50000 each for three years trusting the LIC and the agent aiming at fair returns.But LIC is deducting charges approximately Rs 3000 per year.The current statement says that amount available is only Rs 128000(deducting charges) which means I have lost 22000 in three years from my principle itself.Needless to say no interest on amount invested.If it continues for another 5 years imagine what will happen.I will be getting back 113000, a loss of 37000 for investing in premium institute for NAV of 10.Meaning LIC is taking Rs 37000 from me for keeping my money of 1.5 Lacs for 8 years.Even a bank interest we will fetch 1.5+1.5 lacs for this period.

hello sir

we ordinary peoples getting information form LIC agents and their sub agents regarding new policies and other investment schemes. when hearing their words we are interested to invest our all money and we believes their words also, and it is leading to misunderstandings. so when launching new policies or other schemes publish all policy related clause in news papers in local languages LIC directly.

Sir,

I have invested Rs. 25000/- per year ( 3 Years) i.e. Rs. 75000/- in welth plus Plan (LIC), and the LIC has sent to me statment. In that statement it is found that the amount calculted by me only Rs. 69000/-.

sir,

i invested Rs.75000 lumsum in 2010 and i want to know that what is my nav and the face value of rupee is 10.

so please tell me the NAV value.

thank you.

Reply

Hi Hemant Beniwal,

I also invested in LIC welthplus plan in Feb2010 . i paid Full 3 instllments of 50000 for three years .can you please suggest what should i do.

should i withdraw some amount or now to wait policy term complete.

What is current Nav ,currntly market touch 21000

Regards

Santosh

hello sir

I have a wealth plus investment policy. recently I checked the NAV ,the increasing rate is very low comparing to other policies.if the situation continues, what amount I will get last time? or is it advisable to that surrender my policy?and what amount will get if surrender

Oh! LIC’s wealth plus product is nothing but a big trap for the people who invested in it. It is more than three years since its launch,but still the nav remains at the level from where it started or less. Neither one can withdraw or surrender,lest there will be huge loss. People joined this product thinking that it is launched by LIC and at least one can get the base value. Everybody has burnt his finger by investing in such a unproductive venture. Disgraceful!!

Dear sir,

I have purchased lic welth plus policy and Rs 50.000.00 paid as one time.

Now three years passed Lic promised to pay hightest nav value in seven years.

Please let me know What is the hightest NAV value go after three years passed and

if I have surrender the policy what amount I have receive from LIC.

Sir,

If it is of urgency and we have to break or surrender the wealth plus policy after 3 years, is there a deduction or we atleast get back the sum we eventually invest??

I feel like i have been cheated by my agent.

Sir,

If it is of urgency and we have to break or surrender the wealth plus policy after 3 years, is there a deduction or we atleast get back the sum we eventually invest??

I feel we should not invest in LIC at all. If at all we want to invest then only term plan will be better Jeevan Amulya or Jeevan Amogh. Though premium will be high you will have peace of mind because its with one and only LIC 🙂

dear sir

i’ve already invested in this policy and now feel cheated from the side of agent and want to complaint against him…is anything can be done regarding this matter,

secondly i paid my last installment in 2013 and i’ve invested totally 75,000 in it…how will i come to know when is good time to take my money back…..and what will i’ll get now if i’ll submit my papers…

please help

Dear Investors,

We are talking about only LIC but the same condition prevails with all insurance companies. ULIP introdued by all the Public as well as Private Insurance company is only useful for the growth of their insurane companies and not for the investors. IRDA is closing its eyes on ULIP plans of the insurance companies. I was betrayed by the agents of atlest 5 insurance companies including LIC. I have been paying continuous premium for the past 5 years and still none of Policies could fetch me even the principle amount which I have paid to the insurance companies. I am not able to surrender because I have to pay surrender charges if I surrender beore 7 years. I am actually trapped. IRDA is not bothered about common man. No common guidelines for the charges charged by the insuance companies from the common man.

So, now all of us are sure that LIC (controlled by GOI) is no better than SARADHA & other Chit ( or Cheating ? ) Funds operating in West Bengal. LIC’s agents are misleading commoners the same way SARADHA’s agents have operated; the only difference being LIC’s agents get 4-5% as commission whereas SARADHA’s agents got 25-40%. Poor fellas !!!!!!!!!

It is reliably learnt that these CHEATING MASTERS of the CHIT FUNDS took a leaf of the books of LIC; most of the guys were LIC agents before joining the bandwagon of PONZI schemes.

Hi,

I am having a LIC ULIP policy where i invested Rs 90K for 3 years ,

But now its value id Rs 86k.

As per plan,this amount will be matured after 8 years.

Can you please suggest me whether should i wait for more 5 years or i should invest that money with other plan or so.

Awaiting for your reply.

Thanks,

Rajib

Sir

I have investment 1lack in wealth plus on

12.03.2010 .now this policy passes three year

from the commencement.

Should i surrender this policy.

Kinly clear the confusion.

Sir

I want to know about bharti axa aajeevan suraksha policy which promise return is 8to10% per anum …….

Dear sir,

I have taken a Wealth Plus Palicy of Rs. 20000 PA in 2010 and now in march 2013 , 3 Years will be completed if i withdraw the Policy how much amonut i will get.

Sir,

I would like to inform you that i am very much cheated by LIC agent in Wealth Plus scheme. In this regard i want to know that the how much percentage get returns in wealth plus scheme up to April-2013.

thanking you.

myself invested in lic wealth plus plan in march2010. what is futer for this plan.

thanks.

I have invested in Money Plus (Growth Fund) in Aug-2007. Now i have stopped depositing premium from march-12. till date i have invested One Lac, Now Todays NAV is 12.58, Is this a right time to surrender this policy or will be better to wait for some period considering same amount to invest in Gold.

Please suggest.

I have invested Rs.48000.00 through LIC Wealth plus(sgl. premium) dt 07/05/2010 but now I am understanding that that I was cheated by LIC agent please suggest me economical way out.

I have cheated with LIC agent & invested Rs 48000.00 now how can I econimical wayout from Wealth Plus.

i have paid all 3 premium of 20000/- of wealth plus policy no.444008946,dt.27/03/2010 now i want to surrender the policy so i want know that it would be possible to surrender this policy now or i have to wait for its maturity. pls reply

lic samridhi plus no 496516247 dt-25/4/2011,lic wealth plus no-496015643,dt-4/5/2010,lic market plus-1,no -496008294 dt-19/3/2010.please send present value.

Hi hemant,

i have paid 5 premium of 10000/-out of 6 & last premiun is in month of sept 2012. Pls advice me whether i should pay last one or should surrender the policy.

HI, I AM ALSO CHEATED WITH MY LIC AGENT WITH HAVING A SINGLE PREMIUM OF RS.1,20,000/- IN LIC WEALTH PLUS (HIGHEST NAV IN 7 YEARS) IT WAS PURCHASE ON Feb2010. AT PRESENT NAV IS 9.6766 & UNIT IS 3644.598 !!! MOSTLY PEOPLE BELEIVED IN THE NAME OF LIC OF INDIA.BUT AGENTS ARE MISUSING & TAKING BENIFIT OF GOODWILL OF IT. WHAT SHOULD I DO NOW.IS IT WILL BE RUN CONTINUE OR SURRENDARED.PLEASE SUGGEST.

I had invested Rs.1,20,000/- in the LIC wealth plus in the month of Feb.2010. what should i do now. I wait for good result of surrender the same after complition of 3 years.

please suggest me.

HI, I AM ALSO CHEATED WITH MY LIC AGENT WITH HAVING A SINGLE PREMIUM OF RS.40000.00 IN LIC WEALTH PLUS (HIGHEST NAV IN 7 YEARS) IT WAS PURCHASE ON 13/04/2010. AT PRESENT NAV IS 9.6766 & UNIT IS 3644.598 !!! MOSTLY PEOPLE BELEIVED IN THE NAME OF LIC OF INDIA.BUT AGENTS ARE MISUSING & TAKING BENIFIT OF GOODWILL OF IT. WHAT SHOULD I DO NOW.IS IT WILL BE RUN CONTINUE OR SURRENDARED.PLEASE SUGGEST.

Hi Hemant,

Your post are very knowledgeable & eye opener for many investors like me.

I’m planning to take a policy of jeevan saral.I can pay a premium of 60K yearly & my horizon will be 25 Yrs pls suggest is this a right long term investment.

Else suggest some alternative investment.

Regards

I TOOK A POLICY UNDER PLAN 180-20 IN A SINGLE PREMIUM WITH RS. 20000/- ON 30.03.2007 . WILL YOU PLEASE ADVISE ME WHETHER I SHOULD QUIT THE PLAN OR WAIT FOR SENSEX TO COME UP IN NEAR FUTURE.

good job brother keep it up . . .

thank you sushil

LIC is very bakwas company.don’t trust it. i advice you dont invest in lic.

it will be better to invest your money in post offiice and banks.

sir,

i invested Rs.40000 lumsum in 12/03/2010 and i want to know that what is my nav and the face value of rupee is 10.

so please tell me the NAV value.

thank you.

i invested Rs.40000 in 23/3/2010 and i want to know at present time what is my totat amout.

please tell me the NAV valu.

thank you.

Hi

i have purchased wealth plus when it was launched at feb 2010.Now what should i do withdraw our money of leave it for seven years.Which one is beneficial for me a investor.i have invest single paid premium policy,Please your help me.

i’m planning to take a policy of jeevan ankur or jeevan saral…i’m having a kid of 1 year.i can pay a premium of 20,000/- yearly.plzz suggest which plan i should go for.

Hi Hemant,

Read this – LIC Jeevan Ankur

https://www.retirewise.in/2012/01/lic-jeevan-ankur-review.html

Sir,

I have invest Rs. 25,000/- Per Annum for three yearsm Which one is beneficial for me a investor.i have invest single paid premium policy,Please your help me.

I am very sorry to say that Wealth Plus NAV is negative. When it will +

Hello Hemant,

You have hit the nail on the head. I got suckered into this policy even though I am quite conservative in investing, I asked the some of the similar questions relating the facts you mentioned especially, where and how will LIC invest the money. Now that I understand markets and economy better, I realize it was such a foolish decision to entrust money to LIC. Thanks for educating us all. Keep up the good work.

Welcome Peeyush

Must share TFL with your friends – so that they don’t do such mistakes 🙂

I have paid one time preimum of 7 lacs what I should do? is there a lock in period?

Hi Vijay,

This is a big amount get in touch with some financial planner in your city – he will guide you on this.

What to do , plzz suggest , i already paid 40000/- @ 20k/annum

hii,

I do agree with the narrataion, if it so I WILL WITHDRAW ALL THAT BEEN INVESTED.

Hi Rinku,

Talk to your agent.

HI ,

I am also investing in wealth plus and I have already paid 19 premiums of rs. 5000 out of 36 . Wat should I do . Please guide me as I am naive to all this investing stuff..

Hi Deepak,

Complete the 36 mths period.

hi,

i have purchased wealth plus when it was launched, next premium is pending should i countinue it? how much return i will get at the maturity?

hi sir,

i already bought the wealth plus policy 2 years back means when it was launched. now pls. suggest me my money safe or not? last premium is pending.

Sachin

sir, i have invested 40000 in LIC’s wealth plus in 2010. Is it worth continuing with the policy? Is there any way to get my money back now? If yes, is it worth doing?

Hi Hemant,

I have bought the wealth plus in year 2010 for Rs. 40000/- per annum for three years. I have already paid two installments and third is due on April 2012.

Suggest, should i quit or continue with third installment.

If i quit then what will be the surrender charges.

sir,can u suggest me the place where i should invest or wht kind of policies i should take.should i take any lic policy or nt i too had invested in money plus .if u can give any idea about lic’s any other policy or u can suggest any thing else….

it will be great ful for me…

Hi hemant i have bought lic money plus in aug07 now i want to discontinue the policy what amount will i receive ?or should i continue

Dear Hemant sir,

Thanks for your valuable guidance.

I have invested in LIC, the plan is like….i have deposited 25,000 at the begning and i have to pay 5,000 per year up to 20 years. Agent told me that after 20 years you will get minimum 15,00,000 and maximun up to 20,00,000.

1st thing i want to ask that…is it true? whatever above sated.

2nd thing, if its wrong than suggest what should i do?

3rd thing..what are the options in which we invest and get good return….or i can say that, what is investment and what are the various mode in which we invest.

Thanks

Dhiraj

please advise me whether I should continue with the policy or not. I have taken policy in three installments of 1.5 lacs each. I have only paid 1.5 lacs as first premium. My second installment of premium is due in May 2011. Please guide me if I discontinue the policy how much I would loose or is it worth it now to discontinue the policy.

Hi Raghava,

Better don’t pay 2nd premium – your policy will be lapsed & after completion of 3 years you will get the surrender value.

Talk to your agent – check your policy documents & share updates on ASK US. (don’t allow your agent to trick you again)

Hi Raghava,

Read this:

Surrender:

The policy can be surrendered only during the policy term. The surrender value, if any, is payable only after the completion of the third policy anniversary both under Single and 3 years Premium Paying Term contract. The surrender value will be the Policyholder’s Fund Value at the date of surrender. There will be no Surrender charge. The policy can not be surrendered during the extended life cover period.

If you apply for surrender of the policy within 3 years from the date of commencement of policy, then the Policyholder’s fund value of units shall be converted into monetary terms. No charges shall be deducted thereafter and this monetary value shall be paid on completion of 3 years from the date of commencement of policy.

In case of death of life assured after the date of surrender but before the completion of 3 years from the date of commencement of policy the monetary value payable on the completion of 3 years shall be payable to the nominee/ legal heir immediately on death.

Compulsory Surrender:

The policy shall be surrendered compulsorily in following cases:

i) where the policy is not revived during the period of revival, the policy shall be terminated after completion of 3 years from the date of commencement of the policy or on expiry of revival period, whichever is later.

ii) where single premium has been paid or premiums have been paid for less than 3 years and the policy is in force and the balance in policyholder’s fund value is not sufficient to recover the relevant charges;

iii) where 3 full years’ premium are paid and the balance in policyholder’s fund value falls below 50% of one annualized premium.

The conversion in monetary value shall be as under:

The NAV on the date of application for surrender or on the date when revival period is over (in case of compulsory surrender), as the case may be, multiplied by the number of units in the Policyholder’s Fund as on that date.

When buying term insurance, which is better option? Single premium or regular premium. Isn’t Single premium better as you pay only once when you have cash in hand and do not bother for the term of the policy. With regular premiums, the advantage is that you can simply stop payment and ensure the policy lapses, if you feel there’s no need for cover. The difference in single and regular premiums is almost 50%. What is your advice?

Hi Brett,

Don’t go for single premium – if you compare premiums by time value of money you will find that single premium is damn expensive. (With inflation value of Rupee decreases.) Other reason you have stated is very valid “the advantage is that you can simply stop payment and ensure the policy lapses, if you feel there’s no need for cover. ”

One more point if something happens to insured in initial year of term – I hope you have understood what I am hinting.

dear sir

my self surendra sharma i have investment of (wealth plus) scheme in 40,000 single premum on 19.03.2010 but how to manage it i don,t so please call me at

09977600000pleaseI feel the LIC agents should not be be there. If some are from ur well known circle or family its a pain in throat. I was given policies by agent only after a month and never got a chance to have free look, when I wanted to cancel Wealth Plus. We investors now know of these misguidance, should beware and be cautious ourselves and not repeat the mistake of making money from LIC. LIC should only be for “life insurance” — thats the lesson I learnt.

Hi Amit,

You rightly said “If some are from ur well known circle or family its a pain in throat.” & this brigade is made by all insurance cos. And relative & friends of insurance are called “natural market”.

Absolutely true. LIC should not be taken granted for making good money. It is purely for “LIFE INSURANCE”

I too feel cheated today when got SMS that an amount of 1.01 Lac only credited to my account as against investment of 80K in LIC Wealth Policy 8 years back.

I have decided that from now onwards, not to believe in Agent words who is well known to me since last 18 years.

Hemant,

With SBI , last september 2010 i started smart performer ulip paying 1lac ( supposed to pay 1lac for next two premiums more years) , they write similar to LIC ones mentioned by you, Highest NAV guaranteed.

Could you pls check if this is same case

Hi Varma,

It’s similar type of policy.

Sir, After got cheated by AGENTS of Insurance/Mutural fund, I wake up and acquired some knowledge on how to invest. Am investing in some schemes which i feel fit to my requirement and my monthly budget and earning 8 to 12% per annum. I feel this much return is sufficient. If the Governemnt removes AGENTS/PARACITES Sytem I can get 4% more extra on my investment.

Now also 4% to 5% of my earnings are being transferred to the Agents pockets as commission. We are bound to buy the products through agents only in LIC and Mutual funds. In mutual fund offices if we go directly and apply for a product they should not charge initial charges. But they are receiveing money giving the receipt, after i receive the statement Agents name is appearing. Paracites never leave any opportunity, because they are shameless.

In post offices if we buy 6 years national savings certificate, or 5 year RD, or PPF any thing, if we buy directly the Staff of that Post office giving so many troubles, which means they are forcing us indirectly to come through agents.

Why our hard earned money go to the pockets of Agents. If that 4% to 5% commision not given to agents then we can get more returns. Why governmet allowing/ encouraging AGENTS and commission business.

Why Government making AGENTS as PARACITES like Cycle/Scooter/Car parking contracters. Why it is allowing them to loot our pockets??

Hi Shiva,

It looks that you have faced some severe mis-selling by insurance agent – can you please share some instance so others can be get some benifit by reading your practical experience.

I agree with your points that if someone don’t need an intermediary the benefit should be transferred to investor. Hopefully you may something like this in 2012 🙂

for your kind information now lic agents are become more shameless.they collect cash from uneducated person specially from housewife those are gather money from their daily bazar and agents are investing that money at local market at high interest for 2-3months then they submit to lic.

By this they also earned commission from lic and interest.

IS THIS THE REAL PICTURE OF LIC?????ARE THEY TRAINED LIKE THIS TO LOOT THE INNOCENT PEOPLE????

કોઈ પણ સ્કીમની લોવર લિમિટ હોવી જોઈએ એનાથી વધુ નુકશાન કમ્પની બેર કરે.LIC ટોટલી ઉલ્લુ બનાવી ગયા.મારો સદાને માટે વિશ્વાસ ઉઠી ગયો. Jivan ke sath bhi jivan ke bad bhi.ઉલ્લુ બનાવવાની સ્કીમ

Cheated more than “Saroda” and “Rose Valley” in Kolkata. LIC lost trust of people by any means. People should not trust any agents in financial, insurance and banking market. Just look for savings account and fixed deposit, do not jump for high return which has no trust. Otherwise, just buy assets that can give good return, like buy land.

What happened Mr Bose?

hi didnt want to point out but u hv mentioned bima gold which is a money back policy instead of bima plus which is a pure ulip….no hard feelings pls..any admired article as usual…

Yup 🙂

You got it man – thanks we have edited.

It is true that the agents are making guilible fools of uneducated persons. But I feel LIC is also knowingly supporting these adverts. You walk in at any of the LIC offices and you will find the leaflets strewn around. If LIC really wants to stop fooling clients then they should first remove these leaflets from their premises. And take some action against the erring agents (which I know is a pipe dream).

@ Ajeet

We agree with you.

But even investors are at mistake – they run 24*7 to earn money but not even give 24 minutes to learn how to manage it.

Sir, I have started the policy by 40000 on 20-03-2010 at present how many money i get…

You must be having approx 3411 units. Multiply that by the highest NAV as of maturity of the policy (currently it’s 15.42) which means you will get somewhere around 52 to 54 thousand. Mind you, some tax (TDs) will be deducted at source. So this amount will go.down by few thousand bucks. So effectively you will get approx 50 to 53 thousand. Hope this answers

Can we see anywhere how many units LIC has bought for the particular Policy?

Hello

I think calculate only first 7 years.

Hello Sir I have started the policy by 60000 on 12-02-2010. at present how many money i get and how they calculated the value.

Hi , I have also invested 50000 on march 2010. How many units I have ?

How to know…

Sir, if you go to your account in licindia.in you can see the number of units you have.

For example: I invested 2000 per month for 3 years from year 2010 totally 72000 Rs. Now, I have 6180 units and NAV is 15.32 so I will get Rs.94000 (after tax deduction I am not sure) next week March 2018.

After seeing all comments, I think I am lucky to at least get my money back… when I took policy that agent said I will get minimum 2 lacs because market is growing strong.

sir how you calculate 3411 units

i have invested 50000 so as per this how many units i have..

sir how you calculate 3411 units

i have invested 60000 so as per this how many units i have..

Sachin,

You can check it in licindia.in inside your account.

I invested 2000 per month for 3 years from year 2010 totally 72000 Rs. Now, I have 6180 units and NAV is 15.32; so approx for 60000 you will get 5000 to 5250 units or something .. Sir I am not a consultant.. I am giving only approx value based on my account.

How you say investors mistake, these west LIC agents and LIC people how they are looted from innocent investors. Now peoples are aware and they are not trusting on LIC.