Last Updated on April 10, 2026 by Hemant Beniwal

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” – Albert Einstein

What’s the one thing that separates people who retire comfortably from those who struggle?

It’s not a higher salary. It’s not a lucky stock pick. It’s not even brilliant timing. It’s the boring, unglamorous habit of investing regularly, month after month, year after year. No drama. No excitement. Just discipline.

In 25 years of advising, I’ve never met a wealthy person who got there through a single brilliant trade. But I’ve met hundreds who got there through consistent SIPs that they started and simply never stopped.

⚡ Quick Answer

Regular investing through SIPs works because of three forces: the power of compounding (your returns earn returns), rupee cost averaging (you buy more units when markets are low), and behavioural discipline (it removes emotion from the equation). A ₹10,000 monthly SIP at 12% for 25 years grows to over ₹1.8 crore. The key isn’t how much you invest. It’s that you never stop.

Read More – Aligning Investing with Life Goals

Why Regular Investing Beats Everything Else

1. Your Savings Are Already Monthly. Your Investments Should Be Too.

India is a country of savers. We save almost 30% of our income, among the highest in the world. Our income is monthly (salary, rent, interest). Our expenses are monthly (EMI, groceries, school fees). Our budgeting is monthly.

But when it comes to investments? Most people treat it as a once-a-year, last-week-of-March panic exercise. They dump money into tax-saving products in February and call it “investing.” That’s not investing. That’s tax management disguised as a financial plan.

The best time to invest is when you have surplus money. Since surplus comes monthly, investments should be monthly too.

2. The Double Benefit of Investing Immediately

When you invest the moment your salary hits your account, two powerful things happen:

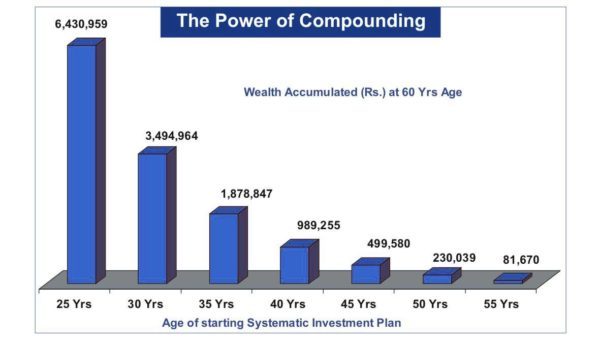

First, your money gets maximum time. And time is the most powerful force in investing. A rupee invested today has 30 years to compound. A rupee invested next month has 29 years and 11 months. That one month’s head start, repeated every month for decades, creates a massive difference in your final corpus.

Second, you stop overspending. When there’s excess money sitting in your savings account, it gets spent. On that phone upgrade you didn’t need. On that impulsive online order. On eating out because “we deserve it.” If the money is invested before you see it, you can’t spend it. Simple. Effective. Life-changing.

Must Check – Every Investor Should Know The Two Poisons of Investing

The Power of Compounding: Let the Numbers Speak

Let’s see what ₹10,000 per month at 12% annual return does over different time periods:

| Time Period | Total Invested | Value at 12% | Wealth Gain |

|---|---|---|---|

| 10 Years | ₹12 Lakh | ₹23.2 Lakh | ₹11.2 Lakh |

| 15 Years | ₹18 Lakh | ₹50.5 Lakh | ₹32.5 Lakh |

| 20 Years | ₹24 Lakh | ₹99.9 Lakh | ₹75.9 Lakh |

| 25 Years | ₹30 Lakh | ₹1.89 Crore | ₹1.59 Crore |

| 30 Years | ₹36 Lakh | ₹3.53 Crore | ₹3.17 Crore |

Look at those last two rows. You invested ₹30 lakh over 25 years and it became ₹1.89 crore. You invested ₹36 lakh over 30 years and it became ₹3.53 crore. The extra 5 years nearly doubled the corpus while adding only ₹6 lakh more in investment. That’s compounding doing its magic in the final stretch.

The New Savings Formula

Most people follow this formula: Savings = Income – Expenses

Change it to: Expenses = Income – Savings

Pay for your retirement first. Pay for your future goals first. Then spend what’s left. This one shift in mindset, if you follow it for 20 years, will change your financial life more than any stock pick ever could.

Ready to start but not sure where to invest?

A structured financial plan matches your SIPs to your goals, risk profile, and time horizon.

Where Should You Invest Regularly?

For short-term goals (1-3 years), recurring deposits or debt mutual funds work well. But for long-term goals like children’s education, retirement, or wealth creation, equity mutual funds through SIP are the proven path.

Equities are volatile in the short run but have consistently beaten inflation over the long run. Traditional instruments like bank RDs and post office schemes fail to beat inflation after tax. If your goal is 10-15 years away, equity SIPs give you the best chance of building real wealth.

Read – Types of Mutual Funds in India: Complete Guide

What Nobody Tells You About Regular Investing

Here’s the paradox of SIPs that almost nobody discusses.

SIPs work best when you’re losing money. Yes, you read that right. When markets fall, your SIP buys more units at lower prices. Those “extra” units purchased during crashes are the ones that generate the most wealth when markets eventually recover. The March 2020 crash terrified everyone. But SIP investors who continued investing during that period saw some of their best returns ever in the following 2 years.

The problem? Most investors stop their SIPs during crashes because it “feels wrong” to keep investing when everything is falling. This is exactly backwards. Stopping your SIP during a market crash is like cancelling your gym membership because you gained weight. The crash is precisely when your SIP is doing its best work.

The investors who build the most wealth aren’t the ones who started at the right time. They’re the ones who never stopped.

The journey of ₹1 crore starts with a ₹10,000 SIP

Start today. The best time was 10 years ago. The second best time is now.

Frequently Asked Questions

What is the benefit of investing regularly through SIP?

Three main benefits: compounding (your returns earn returns over time), rupee cost averaging (you automatically buy more units when markets are low), and behavioural discipline (it removes emotion and procrastination from the equation). Together, these three forces turn small monthly amounts into significant wealth over 15-25 years.

How much should I invest in SIP per month?

Start with whatever you can afford consistently, even ₹5,000. The amount matters less than the consistency. As your income grows, increase your SIP by 10-15% annually. A ₹10,000 monthly SIP growing at 10% step-up annually can build a significantly larger corpus than a flat ₹25,000 SIP over the same period.

Should I stop my SIP during a market crash?

Absolutely not. Market crashes are when SIPs do their best work because you’re buying more units at lower prices. Stopping your SIP during a crash locks in the psychological damage without getting the recovery benefit. Continue investing and let rupee cost averaging work in your favour.

Where should I invest my SIP for long-term goals?

For goals 7+ years away, equity mutual funds through SIP are the most effective vehicle. For goals 3-7 years away, balanced or hybrid funds work well. For goals under 3 years, stick to debt funds or recurring deposits. The instrument should match the time horizon, not your current market sentiment.

Wealth isn’t built in a day. It’s built every month, quietly, through the boring discipline of investing regularly. The magic isn’t in what you buy. It’s in the fact that you never stop buying.

Do the Right Thing and Sit Tight.

💬 Your Turn

How long have you been running your SIPs? And have you ever stopped one during a market crash? Share your experience in the comments.

Hi Hemant,

I want to invest through SIP in some 4-5 mutual funds. How to make such investments on line?.Briefly let me know the easy procedure I have to adopt, scince Iam a beginner in this field. total 4-6 thousand per month

With Regards

I want to invest in SIP Mutual Fund.

Hi Hemant,

I want to invest through SIP in some 4-5 mutual funds. How to make such investments on line?.Briefly let me know the easy procedure I have to adopt, scince Iam a beginner in this field.

With Regards

I am 31 years, in bangalore working as a software engineer and have an earning around 70k per month. I have taken an LICof 15 lakh and invest in PPF and Reliance Tax Saver option-Growth Plan. Last month I started investing in HDFC Top 200(2000 per month). I was considering to invest in the following:

Midcap :

IDFC Premier Equity Fund – Plan A – Growth or sundaram bnp paribas midcap fund

Large Cap

DSP BlackRock Top 100 Equity Fund – Growth or Franklin India Bluechip Fund – Growth – Growth .

Please let me know

1. if this is a right time to invest considering the market volatility. Should I wait for some more time berfore investing?

2. Which of the options should I proceed with for each mid cap and large cap.

Thanks.

Hi Seemanth

Investment in equity mutual funds is done via SIP to meet your long term goals.Once SIP is started it has to be continued for more than five years.In the short term there may be ups and downs in your returns but if you remain invested for a long time you are likely to get around 12% annual returns.In fact SIPs work best during market volatility.All times are good for investing through SIP mode.Growth option is best for wealth creation.

Thnxx Hemant,i will follow your suggestions.

Hey Hemant,

I want to save for Sons Education for which I have 17 yrs & tgt amt is 70 lacs kindly suggest me a SIP for the same?

Hi Hemantji

I would like to invest in SIP for long term for the future of my children. I wish to invest rs 10000 per month. pl suggest in which sip should i invest, and should i take the dividend route or the growth route.

Hi Dinesh,

Check this

https://www.retirewise.in/2011/02/systematic-investment-plan-mutual-fund-sip-best.html

Hi Sneha

You have not mentioned how much you can invest per month.Depending on the amount you can invest in two or three diversified equity funds with good present and past performance.However, after investing keep tracking the performance of your funds on regular basis.You can also check the link given below by Hemant for Dinesh.

Thanks Anil,

I can start an SIP for 2000 and can gradually increase the same. Also i have invested in SIP of like DSP BlackRock Top 100 Equity-Growth, Birla Sun Life Frontline Equity Fund Plan A -Growth and Reliance regular savings equity fund – GROWTH OPTION for 8 months now. Though these funds have good rating I have not breakeven in the same. Do i still continue the SIP?

Hi Sneha

For your additional SIPs you can consider the following funds :

1 ICICI Prudential Focused Bluchip Equity

2 HDFC Midcap Opportunities

3 UTI Opportunities Fund

You can wait for around three to four months. After that check the performance of the funds in your portfolio by comparing with peers and benchmark index and exit the funds having consistently poor performance.

Hi.

I liked ur article n uderstood many thngs from it …

But my question is that investing 1000 or 2000 in SIP is enough or someone should invest more … and it is a tax saving also or not …

And during buying a plan what are the things we should keep on mind .

Thanks

Gagan

Hi Gagan,

The amount of investment should depend on once goal – if your goals are very small or very far may be this amount will be sufficient. So one should first check what are his goals then see what his existing investments are & after that should calculate that gap or how much he need to invest per month or per year. There are special funds for tax saving known as Equity linked savings scheme which will give tax benefit under section 80 C. When we are talking about selection of fund on should stick to long term consistent performing funds.

Hi Hemant,

I had go through a lot from your article you publish in your site. There is a lot

to make thing brief to every one . But what i observed as I am regular visiting you site since last 9 months on behalf of that still Iam not able how to decide or make a bench mark to purchase a fund which will full fill my financial requirement.

For Example:- I read you SIP article.

Every thing is in brief but how a novice consider that he should use this fund for SIP investment. Or he should consider a advisor / broker to begin this type of investment.

Hi Munish,

I will write something on this but that does not mean you should not hire an advisor.

Hemantji,

I started Sip in HDFC Top-200(G)

Principle Emerging Blue Chip Fund(G)

ICICI Pru Dynamic Fund(G)

Sundaram PSU(G)

Raliance Growth(G) Schemes Rs.2000p.m

My Horizon for investment is 6 Years & i want to start a SIP of Rs.1000p.m in Axis Tripple advantage Fund(my one time inv.Rs.25000 @NFO)

Can i achieve my Goal of Child Education (which is in 5 th Std. now) ?

Pls suggest me that i can start a SIP with AXIS

Haresh Soni

Hi Haresh,

I don’t think you should start SIP in Axix Tripple Advantage bcoz even your existing portfolio need changes.

I started SIP few months back (1000 Rs. monthly HDFC tax saver and 1000/- monthly ICICI PRU tax plan), how much return I will get after 10 yrs, please advise of index fund and diversified Mutual Funds

Hi Jitendra

Equity linked savings scheme (ELSS) is the best tax saving instrument, with added advantages of Systematic Investment Plan. If we assume a return of 15% in next 10 years your end corpus will be approximately Rs 5.5 Lakh out of which your contribution will be Rs. 2.4 Lakh. Keep an eye on New direct tax code as it is expected that ELSS will not be a tax saving instrument after that. I will suggest you to go for diversified equity fund as still India is in developing face & fund managers can find good companies that can substantially outperforms the market – so they can generate better performance than the INDEX. You can invest in DSP BR Equity or Reliance Regular savings fund. Index funds & exchange traded funds are good for developed markets as outperforming market is very difficult in these places. So for investor, reduction in cost is important.

Which is best short term regular investment plan?

Thanks for nice article.I understood that it is best way to invest in SIPs.

But I have not yet started.How to start investing in SIPs?

Can you please suggest some best SIP plans for me?

@ Ravi

Hire some advisor he can guide & help you in starting your SIP.

There is no fund or sip which is best – we all know best after postmortem of past performance. 😉

Choose any 2 good consistent funds(not best) one large cap & one mid cap and start your SIP.

Hi..Im saving 25% of my income through SIPs. It gives me a sense of security and guarantee. Also it keeps a check on my expenditure and forces me to plan the expenses. Im not sure whether Equity Mutual Fund is the best way to invest but investment as a concept no doubt should be followed by all.

@ Ashish

You are on the right track, keep going.