Many of us face this dilemma – “Should I use surplus money to pay off existing debt or should I invest?” It is not an easy decision to make. But give me an answer – why someone should take a car loan at 11% when his Fixed Deposits are just earning taxable 8%. 11% vs 6% tax-free (depending on tax slab) = –5% (on 5 lakh loan losing 25000 yearly) – it’s a simple calculation but I have seen n number of people doing this mistake. But in other cases calculations are not so simple…

My Sister’s Story

I am writing this because I want her to read.

Let me first clarify I don’t give financial advice to any of my relatives or friends – I don’t want to mingle personal & professional relationships. I advise them to get in touch with some financial planner or I connect them with someone. Even in the case of my sister I asked her to take help from some professional.

My sister & brother in law earn more than Rs 75 Lakh a year but are not able to save a fraction of this amount. I feel bad about that because I claim that I am doing something in field of Financial Literacy but my family members seem to be financial illiterate. (in hindi “diye tale andhera”) They are not spend thrift (at least they feel) but there problem is very common – LOAN.

A couple of years back they hired a financial planner (I recommended the name & I know he is good at his job) & he presented the harsh reality through the plan. They were not able to swallow what he recommended but still followed his suggestions for couple of months. But as they say old habits die hard – they soon lost the track & blamed the financial planner for that. (this is the irony of planners life)

Idea of this article generated from what they did this month. They prepaid (Rs 10 Lakh) part of their home loan – I should be happy about that but I am not. I have no doubts that they will feel relax as their debt burden is reduced but I know once this loan is finished they will go for another – property or car. I think they should have done the calculation before taking decision + also looked at other factors. Financial assets are must for survival & achieving goals.

Sorry Manya but it’s high time. 🙂

Steps to take and factors to consider before you make the right choice

List down your debts

List down all the debts that you have either in an Excel spreadsheet or on paper. Write down the debt amount, interest rate and duration for each loan. Indicate if any of the loans qualify for tax deduction. For example, if you have taken an education loan either for yourself or your spouse or child, the interest payable is eligible for tax deduction. The principal and interest amount in a home loan availed of is eligible for tax deduction.

Do you have an emergency fund

Check your cash and bank balance. Do you have money to take care of emergencies, unfortunate events like medical issues, job layoffs etc. The amount should be equivalent to 3 to 6 months of your expenses depending on your lifestyle and family situation. (if you are single bread winner go for 6 mths) If you do not have enough emergency fund, use some of the surplus amount to manage that.

Calculate

Check the interest rates. Normally the personal loans or credit card debt have higher interest rates and are basically consumption oriented. It is best to pay off these loans first as the interest would only be eating into your savings account and you do not build any asset with these loans.

I got this email from citi bank – I don’t know any investment which can beat this rate.

Pay off strategy

You have to compare the interest amount you save when you pay off the loan versus the after-tax returns you generate (plus tax benefit on EMI) to decide whether it is better to pay off the loan or use it to save on tax. If you decide not to pay off, the surplus amount can be invested which will also give you returns or increase your wealth. If you take a home loan with the following details –

Loan Amount

Rs. 20,00,000

Interest rate

10.50%

Tenure

10 years

You will have to pay an EMI of Rs. 26,987 per month and over 10 years, it will be Rs. 12,38,440. If you have a surplus amount of Rs. 2,00,000, 2 years after the loan tenure started, you have two choices –

You can pay Rs. 2,00,000 at that time. This will save you Rs. 2,32,000. But you will lose some amount eligible for tax deduction.

You have the option of investing Rs. 2,00,000 in a large cap equity based Mutual fund, you could have earned returns around 10-12% and the total investment would be worth more than Rs. 3,20,000 (even if returns are taken at 12% p.a.). Though returns are not guaranteed, if you have the ability to take risk and tolerance for risk, you might be better off investing in equity mutual funds in this scenario.

Calculators

So actually you have to do a calculation at your end that how much return I need to generate to beat what I am paying as interest. We have added a couple of calculators on our website – these can help you taking important decisions on loans. financial planning

But suppose it is a credit card loan, the interest rate is high and you have to pay other fees and you might end up having an expensive loan. It is better to pay off the credit card dues with the surplus amount.

Emotional Aspect

It is important to consider your emotions. What do you like more – Being debt free or taking some risk by using the surplus to invest in some assets which might give you better returns. If you are not a good saver (my sister’s case) – it’s good to continue EMI (because it’s compulsory) & try hard to save (which is optional). THINK

You should know your risk taking ability and tolerance. Would you feel awful, if you realise later on that the equity markets or any other investment that you understand did very well and you would have made much more money investing there than paying off debt? Consider your personality and emotions before taking the decision.

Pay off debt Vs invest

To conclude, I would like to say that it is better to pay off debts that are costly to service. Paying off debt saves money. At the same time, it is important to invest in assets to generate returns and build wealth. You should use some of the surpluses to pay off loans like personal loans and invest the remaining amount in assets that give optimum returns depending on your risk profile and financial goals.

Pay off the smaller loans first so that you feel good about these wins.

Will love to hear if you have ever faced such dilemma.

The medical profession is held in awe and respect across the globe. It is a noble profession as doctors try to heal sickness, diseases, treat physical and mental trauma.

Acquiring a doctor’s degree is the result of years of hard work in academics, many years of training, and spending huge sums of money. Usually, a Bachelor’s degree in medicine takes about 5 years. But in today’s world that might not be enough to have a successful career and many opt for a Master’s degree like an M.D. which usually takes another 3 years. And then specialisations in various fields. Some might want to do specialized courses which again take time and are expensive. Some might pursue studies abroad which mean higher investment. Doctors also need to keep updating their skills and educating themselves. So compared to other professions, a doctor invests a lot in his career and starts earning properly a little late in life.

Doctors might start earning properly after the age of 28-30 years which is late compared to other professions. A doctor can either begin his career by assisting another doctor or working in a hospital. This means he begins on a regular salary late and hence his social life and events also get delayed. A late marriage, a late kid, and long erratic working hours do influence his financial life. He does not have much time to concentrate on planning his finances. Earnings peak between 40-50 years.

Doctors have the advantage of continuing their practice for as long as possible. But this depends a lot on their reputation and health. Business does go slow for some doctors or starts cooling down once they finish some years in the business. Younger doctors get more popular, they are more in tune with current trends in medicine and lifestyle. Some of them have more specialized degrees. A doctor therefore cannot be lax imagining that he has a very long career ahead of him. He should have a retirement age in mind and plan according to that. If he can continue even after that age, he should consider it a bonus or can decide the terms and conditions of his work which is a great advantage to have.

Doctors love Real Estate 🙂

Many doctors in India invest in real estate for housing and setting up a practice. They are generally overweight in real estate which might not be a good idea. They have to understand real estate is one of the asset classes – so there will be periods of outperformance & underperformance.

Doctors have to decide whether they want to set up their own practice or work in a hospital or do both. Some also want to start their own hospital which means they are getting into a business, which is a different ball game. They need to see the pros and cons of each option and decide which works best for them. If one feels, he is not financially savvy but good in medical skills, he can set up a small private practice and be a consultant doctor in hospitals. Setting up a practice is not easy. In big cities, there are numerous doctors and each is competing for the same target market. Doctors face cut throat business wherein they start charging lower or gang-up against new doctors.

If you are a doctor setting up a new practice, you should devote time to starting the practice and it should start before you finish your previous employment (if your current employer allows this) if any so that you have a steady source of income. You can partner with a finance expert to understand the financing aspect of the business. You need to calculate how much capital you will need for setting up a practice and consider things like space required, where to set up the practice, cost of space, services offered, etc. List the revenue and expenses to find out what will be the status of cash flow. You should constantly upgrade your skills and offer innovative and honest services to customers so that they will be satisfied with the treatment that they are receiving.

When Husband & wife both are doctors (assuming practice)

Many times, both husband and wife are doctors. They are self-employed professionals who earn well but would not have done any financial planning. This could be because they do not keep a check on how much they earn (monthly earnings would be variable) and personal expenses and professional expenses get mixed up. They do not understand investment planning, tax planning, etc., and end up making wrong investment choices or evading tax by hiding income. Many are so busy with erratic hours that they don’t have the time or inclination to spend time managing finances. Such doctor couples need to take the following steps –

Separate out personal and professional expenses

Create a budget

Create an emergency fund

Get insurance cover for self and family so that personal goals and professional expenses get paid off in case of unfortunate events

Make financial goals like children’s education, retirement plans and work towards achieving them by investing properly and reviewing investments regularly.

They should take the help of a financial planner if they are not comfortable doing this on their own.

Doctor’s Financial Quotient

Doctors are very intelligent. Some of them, therefore, think they can make great financial decisions too. But many of them make mistakes leading to financial losses. For example, many doctors do not buy enough insurance at the right time to cover them and their family. They realize later in life that their finances are not well-managed. Buying insurance when you are older is expensive. Some doctors do buy life insurance but ignore disability insurance. This will hurt the finances of the family.

Some of them are in huge debts due to student loans or loans taken for setting up their practice. They are not sure on how to manage these loans. Doctors’ services never go out of demand whichever way the economy is going. Therefore they can afford to take higher risks in their investment portfolio. But many of them are not aware of this and over-invest in low-risk-low returns products. Some of these products might have been mis-sold to them by agents who know their ignorance about such matters – like child future plans & pension plans. If the doctor does not have the time nor the inclination for financial planning for doctors, he should invest in having a good financial planner who can manage his finances and give him sound investment advice as per his needs and goals.

Financial Planning for Doctors

Doctors should take the following steps to ensure that their finances are in a good condition-

They should not be tempted to splurge once they start earning money. Some of them feel they missed out on opportunities to have fun as they spent many years studying and started to earn well much later in life. They splurge on fancy vacations, new cars, eating out etc. It is important to keep a check on expenditure and concentrate on savings and investments.

They should ensure that they have adequate life cover and disability insurance cover so that the financial needs of family and profession are taken care of in case of unfortunate events

Decent indemnity coverage is a must. (I will write a separate post on this)

In some cases practice is their biggest investment doctors have – you should know how to nurture, grow, save & ring fence that.

Doctors have a very busy schedule. They are also called in for work many times post-work hours. Apart from this, they have to manage family, health, social engagements etc. It is important that they have a proper fitness schedule. They have to eat right and exercise so that they are in good physical shape. They need to switch off from their work every day for some time and pursue what they like so that they are mentally fit. This is important for sound financial health.

They have to make a financial plan the plan should have financial goals listed and they should execute the plan to achieve these goals. If they do not have time to research and make one, they should hire the services of a financial planner. [hope doctors understand importance of professionals 🙂 ] They need to have a proper investment plan. They should invest in a variety of assets including equity, mutual funds and debt so that their investment portfolio is diversified and they get optimum returns and long-term capital appreciation. They should ensure that their debts are not beyond their means.

They should pay off education loans taken and only then go for home loan or loans for buying property to set up the clinic. They should ensure that they understand their investments and performance of the investments rather than blindly following the advice of the financial planner. They should revisit the financial plan regularly and tweak it as per changes in their life situations and macro and micro economic conditions.

They should also invest in themselves by upgrading their skills, learning about latest trends in health care and networking with other doctors and professionals in the healthcare business.

Doctors’ lead busy lives but it is important for them to focus on their finances so that they can grow their wealth, manage their taxes and have a healthy and secure financial life. This is important for a good long medical career as well.

The irony of Doctor’s life

The irony is doctors don’t follow the rules that they establish – first diagnose & understand the problem and then prescribe appropriate medication. But when it comes to finance they prefer over-the-counter products. Many of them buy financial products without really understanding them as they are not in touch with this subject and due to lack of time rely on the insurance agent or the financial product seller who claim to take care of your investments but are just looking to increase their sales.

If you are a doctor – I will love to hear your side of the story.

No one asked major questions when KN Sivasubramanian (53), fund manager & CIO of Franklin Templeton AMC retired last year after working there for almost 20 years. During his times fund performance was beyond any doubt. May be due to history of Franklin Templeton – 70 years of asset management history, presence across world, first to focus on emerging markets, managing almost $900 Billion (almost half of Indian GDP).

Image courtesy of 1shots at FreeDigitalPhotos.net

Let me remind you:

When you should sell your Mutual Funds?

In a nut shell one can exit his investments in mutual funds if:

Your life-cycle stage has changed impacting your risk profile

If the expense ratio of the fund rise

If there is a major change in the attribute of the fund

If the STAR fund manager is changed

If fund is not complying to its objectives as laid down

IDFC Premier Equity Fund Manager Resigned

But when news broke in media that Kenneth Andrade (46), fund manager & chief investment officer resigned from IDFC AMC to pursue “other entrepreneurial options”, the investment community got jitters. I analyzed why investors should be concerned now:

IDFC has very short history of managing retail investors funds (IDFC purchased Standard Chartered AMC in 2008, which had primarily assets in debt oriented funds)

Kenneth Andrade was counted and accorded as star fund manager by the fund house and media.

IDFC Premier Equity Fund was pathetic performer before Kenneth Andrade took the charge and after his handholding it made good returns for its unit holders.

IDFC Premier Equity Fund is the flagship fund of IDFC AMC managing (Rs 7300 Cr – 66% of equity assets managed by IDFC AMC). It overshadowed other funds of its own fund house.

IDFC AMC employees sold Kenneth Andrade’s exceptional performance (in mid-caps). This sales practice harms more when you create demi-gods and gods turn their back.

Let’s look in details at IDFC Premier Equity Fund & Kenneth Andrade contribution in that – before taking any call.

History of IDFC Premier Equity Fund

This fund was launched in September 2005 – launch was no less than a film star launching his son. (marketing campaign created image of supernova being born, in midst of twinkling stars)

Kind of forms that were printed – I have never seen them before or after this fund (printing cost must be at least Rs 100 for KIM) – distributors were given very limited forms. Forms availability was done when the business commitment was taken.

Best story about the fund was that they declared on launch that they will be managing limited assets in these funds & if I am not wrong there limit was Rs 300 cr, which was achieved in NFO. Afterwards in future they managed it like Interval Fund, where they opened window for new investors on Fund Managers call. IDFC sales team exploited it well creating impression of New Fund Offer at every window when sale was opened in the fund. (but there are lot of loop holes in this to accept funds)

Initial minimum investment size was kept at Rs 25000 – normally its Rs 5000 (to make sure its Premier and it’s for Premier)

It underperformed before Kenneth Andrade took over – I still remember one of my friends regularly called it “PunarJanm Fund” in 2006 – highlighting the fact that you invest in this life & returns will be given to you in next life 🙂 [In mid 2006 it was negative 15% since inception – where other mid cap funds were only down by 8% in the same period]

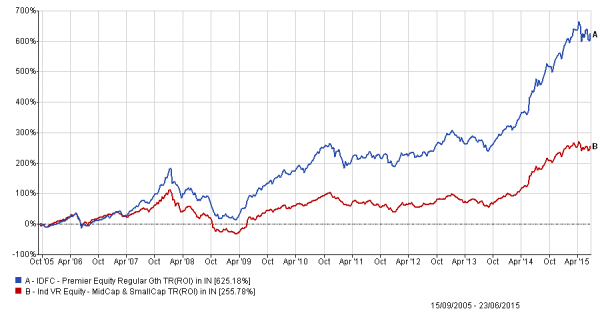

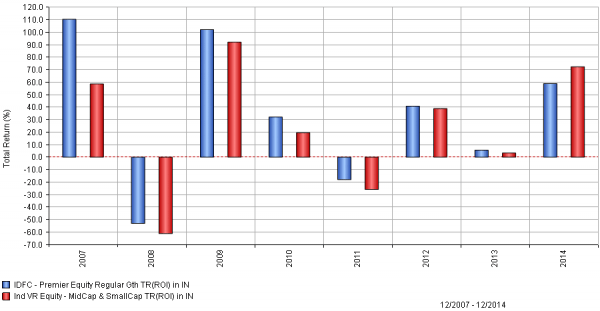

Performance of IDFC Premier Equity Fund

Exceptional performance is visible in above chart – fund generated 625% returns in comparison to 255% by peers. But this gap started building after change in Fund Manager.

Discreet Performance of IDFC Premier Equity Fund

You can clearly see fund outperformed peers in 7 of last 8 years. Important thing to see is outperformance in falling markets (2008 & 2011)

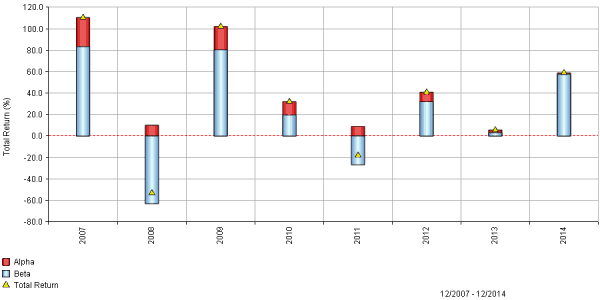

IDFC Premier Equity Fund- Total Return Decomposition

This is the one of the key chart we use before selecting funds – this charts shows if a fund manager/AMC is adding value to a fund.

The chart shows:

Total Return – The Total Return over a discrete period

Alpha – The Alpha over the discrete period

Beta – The Total Return minus the Alpha (the difference)

Reading the chart, you want lots of red at the top of the charts to show this.

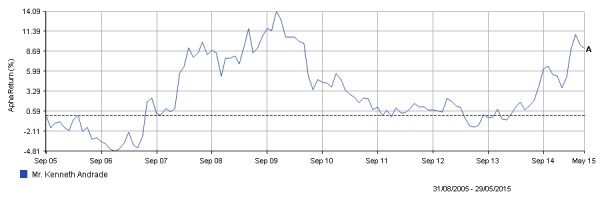

Kenneth Andrade’s exceptional performance

Kenneth Andrade is a Commerce graduate from Mumbai University. Prior to IDFC AMC, he has worked with Kotak Mahindra AMC as fund manager (July ’02 – Sept ’05), SSKI Investor Services (Mar ’99 – July ’01) & (Jan ’02 -July ’02) in Portfolio advisory -Retail Broking Services, Nimbus Communications – (July ’01-Jan ’02) in Broadcasting – Content Development, LKP Shares & Stock Brokers Pvt. Ltd (Jan ’98- Mar ’99) as Analyst -Equity Research, Meghraj Financial Services (July ’96-July ’98) as Portfolio Manager.

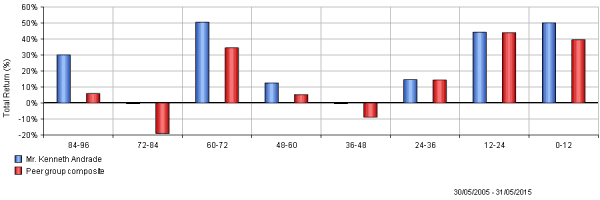

Alpha Generated by Kenneth Andrade (Mid Cap Funds)

Kenneth Andrade Vs other Mid Cap Fund Managers

Kenneth Andrade in bull & bear market

100% outperformance in falling markets is commendable.

What investors should do now?

It’s not going to be a simple decision with your units, that we can use OLX to sell them in haste. These are hard times but with challenges open doors to opportunities.

IDFC has decent equity assets and with this kind of assets they can attract good fund managers from the industry.

A fund manager is face (agreed- a powerful one), but lot of people (co-fund manager, stock selection committee, sector analyst, Independent research units etc) and process (SEBI’s guidelines, fund house internal caps, in house researches, software-both internally developed and hired etc)-are attached to a fund. None of them have moved or could move with Kenneth.

Even if you believe that new fund manager will not be able to match Kenneth – still this existing portfolio should have some power/fire for next few quarters. Wait & watch before taking any action.

Our suggestion is add this to your watch list. Turmoil demands a cool headed decision.

Do you have investments in IDFC Premier Equity Fund or any other IDFC Fund? If yes, share your views or post anything which you feel discussing.

It is well published and we all know that in the past 5000 years of India history, India has never invaded any country. But do you know that out of the that last 5000 years, 4750 years – India’s growth rate (which is measured by increase in GDP or Domestic Product) has been the highest in world. It was only when the British came to India, we saw, India’s GDP going down. NO wonder, India was known as SONE KI CHIDYA.

India called “Sone Hi Chidya” because we contributed almost 30% of World GDP at some time.

Year 1000 (in 1st AD it was 32.9% & currently we hold 7% share on PPP basis)

Once again, we, the Indians are making some big impact in the world’s economy. India is the now fastest growing nation of the world.. & third largest economy PPP basis.

The International Monetary Fund (IMF) downgraded forecasts for GDP growth rate of many countries including China. But it is positive on India. Here are the GDP growth rates of the last few years and forecasts for 2015 and 2016 –

Source: IMF

The important thing to note in this table is that India’s GDP is expected to grow at a higher rate than China. The International Monetary Fund (IMF) also expects good growth rate all the way up to 2020.

India Rise How & When Video

Hans Rosling was a young guest student in India when he first realized that Asia had all the capacities to reclaim its place as the world’s dominant economic force. At TEDIndia, he graphs global economic growth since 1858 and predicts the exact date that India and China will outstrip the US. (India Shining Best Video)

Why is India on this path of good growth?

High GDP growth rate is attributed to many factors –

1) New Government – The government has taken some positive steps for smooth business and better governance. There have been steps towards effective administration, cutting red-tape and improving transparency in government offices. This has increased efficiency which helps businesses as dealings with the government departments are smoother. administrative efficiency helps since it comes after several years of policy paralysis. There have been announcements of many policy reforms which help the economy. For example, it takes 27 days to register a business. The new government wants to make India a business friendly destination and has planned steps to be implemented so that businesses can be registered in one day. Import rules for some raw materials have been eased. The budget announced a corpus of Rs. 1000 crore set up for entrepreneurial units and startups. Yes, there are still hiccups for foreign investment and bureaucracy functioning but these things cannot be changed overnight and there is an awareness and intention to change these issues. There is a wave of optimism within the country as well which makes people motivated to do better in their profession, service and business which contributes to the business.

They also react to changes in the global economy and business. For example, looking at the declining oil prices, the government hiked the excise duty on petrol and diesel to augment its revenues and the additional revenue has been allocated for infrastructure development. Considering that the whole world is going digital, the government has started working towards a Digital India where all government records will be digitized.

2) Steps taken by RBI – The Reserve Bank of India (RBI) led by Raghuram Rajan has also taken fresh steps to improve the banking system and economy. The inflation was very high. For example, Consumer Price Index (CPI) in November 2013 was 11.2% and in November 2014, it fell to 4.4%. Of course the dropping of oil prices also had a role to play in this. The rupee was also unstable before the new governor took charge. Now the rupee has performed better than many currencies. Fiscal deficit is also more in control now. The markets also have more confidence in the new central bank governor.

3) Oil Imports – India’s oil import bill is very high and one of the main reasons for export import imbalance. Now with falling oil prices, inflation has been contained, GDP growth has improved and current account balance in in a better shape. This presents a good opportunity for reform and growth as capital saved on the oil bill can be used for investment in infrastructure and public goods.

4) Demographics – India has the advantage of a young population and a widely educated population ready to join the workforce. This means additional GDP can be produced. The dependency ratio in India is good so there are more people working and lesser people dependent on the working population compared to many other countries. If the young population is trained and educated in the right skills, this human capital can be used in the best manner else the huge population can become dependent on limited resources which is not good for the economy.

Look around you and will realize one more factor which is driving India. This is the youth of the nation. YES, the young India. Do you know, India account for over 25% of the total young population of the globe which is less than 35 years of age and it accounts for more than 60% of our population. Young population not only adds to working population but are the main drivers of demand. just ask yourself, DADA ji jyada demand karte hai ya phir pota – poti.

5) India has maximum number of English speaking person, even more than the entire population of US. No wonder India is becoming a outsourcing center for the globe. The entire world is looking at India to support for their service. A credit card verification in Australia takes place in Jaipur. If you dial railway enquiry number from London, it lands up in Gurgoan Call center. Just Amazing.

5. India is growing on Infrastructure and even if half of the projected Infrastructure projects become reality, it will further give boost to India’s growth. New government is actually talking about laying more roads than built in last 50 years.

The list to India’s growth story is endless and it would takes more space than the entire blog till date.

Let’s quickly see extract from famous report of Goldman Sach “Dreaming the BRICs: Path to 2050” (BRIC = Brazil/Russia/India/China)

India will takeover Japan in 2032 to become 3rd largest economy of the world, just behind US & China.

How to participate in India Growth Story

All I want to convey is that we need to Believe in ourselves. The direct impact of this growth story would reflect in the equity markets and to share this prosperity, you need to partner India companies for long run by way of Equity Investment. Invest in Equity and you will reap the benefits of Indian growth story. In the last 35 years, India’s GDP has grown consistently over 6% and now we are nearing 7.5% GDP growth target. In the last 35 years, stock market have given more then 17% returns p.a. and Rs. 1 Lac invested in sensex is worth more than 2.6 crores as on Today. But the fact that a average Indians have not participated such marathon growth.

In 2004 Election, BJP used this Phrase “INDIA SHINING”.

That was just an ad or punch line but in reality as well, India is Shining. We at TFL, will bring series of articles where we will share information, facts, videos etc on why India is actually shinning and why as an Investor you should be knowing these facts.

To start the series, lets understand the real strength of this economy – the rising of middle class.

By Middle class, we mean what is commonly understood i.e., the Middle Income Group.

This middle class in India is not only just rising but rising at a very fast pace.

India will have more than 80% of its population in this bracket by 2040.Just take a look at the graph below.

*Middle Class: Income between Rs. 3 Lakh – Rs. 15 Lakh(2009-10) Source:Equitymaster

This middle class is not the same what it was just a decade back. They were then branded as a conservative and thrifty people.

But not anymore, India’s middle class is now dynamic, educated, liberal and forms the pillars of this vibrant Indian economy. And why do you think Middle class helps economy to grow? Most importantly, they help in distribution of wealth to many rather than concentration of wealth to few. Now when the wealth gets distributed to many, spending of money or channelizing the money in the markets takes place at a faster pace. For example, all these middle income group people demand goods and services like Fridge, TV, Cable Services, etc . and more demand means more growth for industries and in turn, more development of the economy at large.

It is not a rocket science and we believe everyone can understand that the Indian Businesses which will be serving this large segment of people will stand to gain. Look at the way the software company Wipro has become so big after demand of computer software went up since 1980s. Now the shareholders of the company became wealthy as the business went up. It is sometimes hard to imagine but it’s a fact that Rs.10000/- invested in Wipro’s shares in 1980 is worth more than Rs. 4 crores today.

Now the overall demand in India is rising at a very fast pace whether its consumer durables, garments, Education & what not. Just to give you an example – take a look In 1980s, owning a car was RICH people’s dream and now owning a car(Source: CLSA) is just an ordinary thing in life. This not only helps car manufacturers but so many people get employed, so many other industries grow to support car industry and hence the development takes place.

The speed of vehicle goes up when the wheels rotates at faster pace. Similarly, the speed of the money rotation from one hand to another is the speed of the growth of the economy.

DON’T YOU THINK SO?? Believe in our economy and take benefit from it.Foreigners have understood the strength of India but as we say DIYA TALE ANDHERA; we Indians have yet to realize our fullest potential.

Proud to be among the Indian Middle Class

The dream run is on. All researchers are busy anticipating the time when we would cross the US economy and threaten China. The basic assumption of this research is that India is getting rich. The population has become a boon to our nation (I think Government also agrees, as they are no more showing the legendary “hum do hamare do” advertisements). But is it only the population which will make us competitive economy or there are some other factors also? Population rate is faster in Pakistan but it is on the mercy of the international aid it receives. So only population cannot be the only criteria. So what else? Just look at the below graph.

The population officially is classified into Socio-Economic Classes (SEC). In the above graph, Sec B & Sec C is the middle class. A big chunk of the population is the middle class and this class is reaping the opportunities that the nation is giving. This class is educated as the literacy levels are now 81%. See the figure below.

This middle class is young also. This means that the phenomenon of India enjoying this spending regime would be longer. The country would have more youth and fewer dependents. Young atmosphere creates vibrancy and opens gates for new ideas and contemporary spending. The demanders ask for new and improved things and the cycle of money keeps on revolving. See how the population age graph coverts from a hill shape in 2000 to a dome shape in 2025.

And that not all as on international front also we shall continue to ruin the sleep of BRIC countries, US and UK.

And when we talk about spending the major part goes towards paying mortgage, EMI and rent. 20 % of the earning goes towards buying groceries. The spending on transportation and communication is increasing making India the market of “New Launches”. Clothes and apparels which we did not care in past, now accounts for 10%. Clearly the help from the Bollywood and Fashion weeks seems to be working.

And when it comes to Automobiles, gone are the “Hamara Bajaj” days. Every member in the family wants his own 2 or 4 wheeler. And why should boys have all the fun…..

Conclusion: The Indian Middle class is rapidly increasing its size and purchasing power, and will be an increasingly important force in global economic rebalancing. Indian middle-class clearly has shown that they are on a verge of creating a demand which would be enormous in size. They have highlighted that they want to invest in automobiles, mobiles, credit cards, home loans, holidays, shares (Read: What is Equity) etc. So if you are planning to invest in India, this is the time. The fancy has caught the bigger investors and soon would trickle to small investors. So it’s your turn to earn for the India Inc.

Credit & Source: the graphs and some information have been sourced for the CLSA India Report 2009.

Time has come for us to realize our own potential and maximum benefit from it. Please let us know what do you feel about ‘Indian Growth Story’?

It is very typical in our society. You have been married recently and soon parents, relatives, friends and neighbours start asking you when are you going to be a parent! Parenthood is a big step. There will be many changes in your life from various perspectives. People might say you are being too objective but you MUST consider your finances before you decide to become parents because one might not be aware of costs of birthing, parenting etc.

Image courtesy of Stuart Miles at FreeDigitalPhotos.net

Steps to prepare you financially for parenthood

Save, Save, Save

You have to start saving more each month as there will be a new member in the family and it is your responsibility to provide for the child. There will be many expenses like doctor’s visits, vaccinations etc. with a newborn child and you need to have money for it. You will have enough time to save up a substantial amount if you start now.

Calculate the cost of having a baby and being parents in the first year

Having a baby requires lot of financing. Before the delivery, there will be costs related to the pregnancy, which means regular check ups, medicines and medical tests. The actual delivery and hospital expenses are to be taken care of. Once the baby is home, there will be costs like clothes, medicines etc. There are tools online that help you calculate the cost for 1 year. You can check with friends who have become parents recently or even ask the doctor.

Inculcate better money habits

It is important to start practicing good money management habits if you are not already doing that.

Ensure that you do not get trapped in too much debt. Try to repay some of the costly loans like personal loans.

Build an emergency fund worth 3-6 months expenses so that after the baby comes, if there is an unexpected emergency as well, you are in a position to mange finances.

Create a budget by dividing expenses like fixed expenses (rent, regular expenses), variable expenses (grocery, petrol) and discretionary spending (movies, holidays etc.). Then track your expenses and try to live within the budget.

Keep a check on unnecessary expenditure and make an effort to reduce them.

Plan Ahead

You need to plan certain things. You need to think through certain matters before the baby comes into your life as at that time the baby will be the most important priority for you and you will not be able to think about other things

Live on 1 salary – If both the spouses are working, when the baby is born, one parent will have to temporarily stop working. This is a major financial consideration. Sometimes it will take long to resume work, which means you will have to manage on 1 income. You have to plan on how you will manage.

Check Insurance coverage – Have you taken insurance? Check your insurance coverage and see if it will take care of the additional family member else opt for higher coverage or a family floater.

Leave policy of the company – Look at the leave policy of the company that work in on paid maternity and paternity leaves. Check the company’s stance on additional leave required. Most companies cover medical expenses for 2 children. Check the procedures and terms and conditions regarding the same so that you are not in for any major surprise.

Take care of health – Both parents should take care of their health. It is important that both are fit and do not have health problems. This will lead to physical and financial difficulties.

Do not go overboard purchasing baby stuff

The shops will have lots of nice things to buy and it will be easy to go overboard and buy cute toys, clothes and things. But you have to hold on. A small baby does not need too many things but more of your attention and love and he/she will soon outgrow things. As the child grows bigger, there will be many opportunities to buy stuff and you can indulge in your child a bit by bit.

Make a will

It is important to make a will and make sure it is clear as to who will get what of your assets and liabilities in case of any unfortunate event. The baby needs financial protection for future and you should ensure that you give him/her that.

Have you thought of the financial factors to consider before taking the step towards parenthood? Let us know what kind of preparation from a financial perspective have you done.

Renowned for his analysis on Investor’s behavior in investment field and his long-term stock picking ability – yesterday Mr Parag Parikh lost his life in road accident in Omaha (US) – he was there to attend investors meet of Berkshire Hathaway (Warren Buffet’s Company). I was sad & shocked by the news & not sure how to react – when one of my friend shared this news in the morning, first thing that came to my mind – Life is too short… and indeed a bubble 🙁

He was veteran investor since 1979 & managed investor funds through PMS – in 2013 started PPFAS AMC. He was big fan of Warren Buffett style of investing – which was clearly visible in his writing & asset management. Like to many, he impacted my life & thoughts – his demise is big loss to Indian Financial Industry.

He was different!!

His AMC managed only single fund – PPFAS Long Term Equity Fund – no other equity or even debt fund. And no plan to launch second equity scheme. In a previous interview, he said Asset Management is not a grocery store business. There is just one single way to right investing. You can’t have 20 ways.

Their ads & communication clearly mentioned “Investors should note that this Scheme is suitable for investors who have investment horizon of minimum 5 years.”

Only AMC to conduct unit holders meeting similar to company AGM.

You will be surprised his funds biggest holding is “Google” – almost 10%. I don’t think there is any other diversified fund in India – where you will find international stock in top 5 holdings.

He was the first who talked about “skin in the game” – in Feb 2015 employees held approximately 9% units in the fund.

His Book – Value Investing and Behavioral Finance

(My daughter did her calculation on this page)

I bought this amazing book just before starting my practice – I still remember that I first read this book when I was on the way to Ajmer. I am a slow reader but I almost completed 60-70% of the book in one day trip. This book was published in 2009 & covered markets from starting of Sensex to bear market of 2008. It’s an amazing book on Behavioral Finance & Indian Market History – his ideas & guidance have lot of impact on our practice & TFL Blog.

First Page of His Book – WHY PEOPLE FAIL

When he launched AMC – his words

“For us, mutual fund is not a business, it is a money management profession. We will do things which benefit the clients. Currently, we notice the mad fight for assets under management (AUM) by AMCs, because the profession has become a business. Our foremost goal of getting into asset management, is to make money for the retail investors. I am not concerned if the assets we manage are large or small. We want the investor’s money to be managed in a very transparent manner. More than two decades ago, we started as a broker firm and gradually moved into the portfolio management services (PMS). The mutual fund is a logical extension and transition for us. I genuinely believe that mutual fund is a very good asset class for investors. As we have the expertise in money management, we can add lot of value to small investors.”

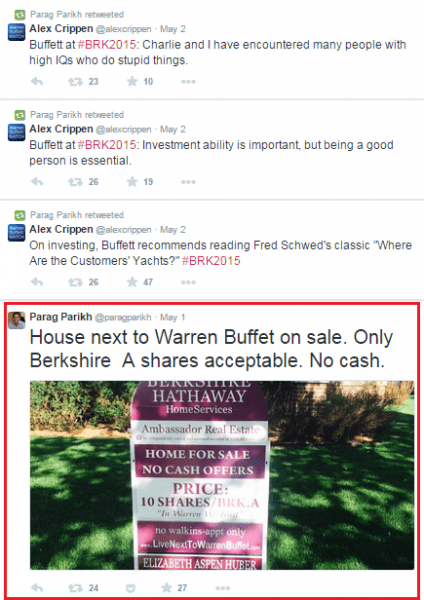

His Last Tweet

Current Price of 1 Berkshire A Share is $ 2,16,000 – 10 Shares Rs 13.6 Cr.

(Overall Gain 1964-2014 – 18,26,163% or 21.6% CAGR)

Parag Parikh, was a flag bearer of value investing, disciplined approach to financial management and penned his understanding in his 2 famous books: Stock to Riches- Insight on Investors Behavior and Value Investing and Behavioral Finance: Insights into Indian Stock Market Realities. Being co-dreamer of the same philosophy Parag was bold articulator of his thoughts on Financial Planning.

His insights, convictions and practice helped change minds and financial positions of lot of investors. His books and views will continue doing so, but I hoped he could continue witnessing such changes… RIP Parag Parikh.

“A ship is always safe at the shore – but that is NOT what it is built for.” who said this?? And is he talking about the ship or something else?? Albert Einstein said this 75 years back but I am sure this can be applied to our life, career & definitely investments.

We invest so that our money earns more money – I think NO. We invest so that we can achieve our goals – now you decide the investments which can help you in achieving your goals. But of course, there is some trade-off between risk and investment returns – mostly higher risks are associated with higher returns or vice versa. (But… – what is Risk?) It is important to understand risk and risk management associated with investments.

If you have to get a job, you have to attend an interview. There is a risk that you might not do well in the interview or there are candidates better suited to the role. So there is an element of risk involved. Similarly, it is difficult to find out an investment option that gives returns with zero risk. When you buy real estate, there is the risk of prices going down or prices remaining the same or you may not be able to sell it when you will require money. When you do investment, risk will be there. It is important to understand the risks involved in different types of investment and decide the most appropriate ones depending on how much risk you can financially take and how tolerant you are to risk. Fixed deposits have a lower risk involved in losing capital or interest rates fluctuation but give lower returns compared to shares of blue-chip companies in which there is a higher element of risk. Someone rightly said, “Doubt kills more dreams than failure ever will.”

Volatility means the value or price of an asset rises and falls sharply in regular intervals. Risk is the potential of loss in investment. High volatility does not mean high risk and at the same time, low volatility does not mean low risk. In the short-term volatility in prices can affect you as if you want to sell and get money in the short term. But if you will focus on the Goals – you will be able to digest volatility to some extent.

Inflation is a risk to investments

Inflation means rising prices. It erodes purchasing power. Savings in your bank account earns 4% per annum. But if inflation is 6% per annum, your savings will lose value every year. The value of Rs. 50000 today will be lower one year down the line and even lower 2 years from today. Investments made for retirement have to be reviewed regularly. If inflation is high, the amount that would be available for you at retirement will not be sufficient to sustain your lifestyle and achieve your goals. You should understand debt will always generate negative returns – after adjusting for tax & inflation. If we assume this return is negative 3% – the actual value (purchasing power) of Rs 100 invested today will only be Rs 75 after 10 years. THINK

There are many unknown factors that can impact investments

There are a lot of views and analyses on the macroeconomic conditions, microeconomic factors, economic growth, and various investment options. These views and analyses help in the estimation of the performance of asset classes. But even if one correctly analyses all these factors and takes decisions, one can never be sure as there are a host of unknown factors that can affect investments. Global financial conditions, conflicts between countries, epidemics, volatility in prices of commodities like petrol can cause fluctuations in the value of investments. There can be a swarm of investors acting in a certain way that causes the markets to behave differently than predicted. It is difficult to predict such conditions and factor into technical analysis. Therefore the risk is always omnipresent in investments. Carl Richards summed up in one line “Risk is what’s leftover when you think you’ve thought of everything.”

Risk can be managed by investing in different asset classes

One way to manage risks in investments is to have an investment portfolio of different asset classes. Depending on investment goals, age, risk capacity, risk tolerance, and market conditions, one should invest in different investments like debt, equities, real estate, gold etc… Each has its own risk element and returns percentage. A balanced portfolio that is reviewed regularly will allow your investments to grow and you can manage risk. Do remember that you cannot eliminate risk but only work around it.

Returns cannot be guaranteed. Moreover, there is always a risk of losing money in investments. Even the “safest” investments have some element of risk. Therefore it is important to create a balanced investment portfolio of savings and investments. Investments should be done on the basis of risk capacity and risk tolerance and they should be managed properly.

Feel free to share your experience & ask questions in the comment section.

Today formidable India will fight mighty Australia – no one can predict the result but let’s hope result will be in our favor. Today everyone will be glued to TV or internet but let’s refresh our memories before that….. Let’s ride on time machine… 2015 >> 2011 🙂

Cricket mania is at its best… Cricket has over shadowed everything…. Other sports, movies, & issues like corruption. No one was bothered about the state elections or finding whereabouts of Shah Rukh Khan. All were glued to the idiot box with a bucket of popcorns. So I will also not break the continuity and will not bore you with a heavy topic, instead would try to connect cricket with the financial world. (This article was published in 2011)

2nd April, 2011 was the day when we got what we desired for so long. Our generation has grown seeing the video footage of Kapil Paaji, dressed like a gentlemen, lifting the cup and then the champagne raining from the balcony of the Lord’s. Now Dhoni has given us one more such memory and this is special as we have seen this team growing from bottom to the top. These “men in blue” really showed that with a strategy in place (Viru said that this Team was already working on the World Cup since last one year but we know they were planning from at least 4 years), and discipline you can change the fortunes.

Let me take you to the Financial Planning learnings from this World Cup Final win:

Setting Goals: After losing match Sangakkara said “I think if you need to win against India you have to score 350”. Well what he said is life. “You need to plan and plan extra for what you have not planned”. Although I am sure that Dhoni that day would have challenged 350 too, with the form the team was in but in our life we must make a financial plan to achieve our goals.

Asset allocation and Diversification: Sreesanth played poorly but his performance did not impact India as much, as others contributed well. A player is like an asset and you need to pick a right combination. Diversification benefits if one asset is out of form or flavor.

Short Term Performance: Zaheer Khan gave too many runs in last overs & Sehwag got out for a duck, but that doesn’t mean they are not good players. So, we can’t judge them by single match performance. Similarly you should not judge investments on their short term performance. Give them a suitable time and their justified cycle.

Beware of Mis-selling: There was some sort of cheating in the toss as Michael Vaughan said on his twitter “Sangakkarra has stuffed Dhoni… He shouted tail in the 1st toss and lost it …You can hear it in on air,” Sometime even before you start investing people will cheat you, mis-sell you. The way is to beware of the cheats and take a corrective action. You simply can’t fold your hands and surrender your financial life to the sharks. You need Fight till you have a plan which you are confident that your financial goals would be achieved.

Role of a Coach: You would be lucky if you saw Gary Kirsten laughing. The man is so miserly at even giving a smile. Gary Kristen was not playing but we know he was the “Krishna” of this world cup Mahabharata. The rule in financial planning is that, someone needs to decide and take action. And one can only decide if he has the full knowledge. If you feel you do not have the proper insight or know-how of this financial world get a Coach. And he is your Financial Planner. By the way, Financial Planner also may have a frowning face and bad sense of humor but I know they feel happy when they see their client is enjoying his financial life.

Predicting patterns: People try to predict future too much by looking at past. Before match started media started its DARAO kind of coverage–Host nation never won world cup… If Sachin makes a ton India will lose…. After losing toss – team batting first won 80% of the finals …. After Sri Lankan inning – no one ever won world cup chasing 274… blah blah. Similarly people try to find patterns in equity markets. If history would have repeated every time, what is the thrill in life than? Learn from History but do try to make it a Science and start taking it as a basis of your decisions.

Inspiration: This cup was for Sachin. Thousands of eyes got wet (including mine) when Virat said “he has carried Indian cricket for 23 years, and now it was their turn”. Sachin was not able to contribute much in the final but he was the backbone. In life also and particularly in Financial life we all should have inspirations. Our financial decisions will make or mar the lives of our dependent, so next time if you are still lazy to put your financial plan in place, just look at your family and draw that necessary inspiration.

Eyes on goal not on the score board: The start was bad for the Indian innings, but Virat, Gambhir and Dhoni had eyes set on the goals. They were not looking at score board after every ball they were just playing to win it. In our life too, we may win or lose in short run, but confronting it on constant basis is a futile exercise. When you sit with your financial planner, the goals are drawn and strategy is in place, chasing markets is a waste of time. These should be non-events and believe in your Financial Coach, that he would provide the extra cushions, in case you need them.

Take Responsibility: More than the World Cup Win, Dhoni’s respect as a man has gone manifold just because of one brave decision and that was to promote him up in the batting order and face the Lankans. Just imagine the pressure he was in when he came in to bat in front of the 6.5 crore pair of eyes watching him. Thriller…. Dhoni is the captain of Indian team & you are captain of your family – so take responsibility. You are the asset creator and manager of your family – understand this. On the field or off the field take wise decisions. Some of them are hard, like paying for a Term Insurance, despite knowing that you are young to die and will not get anything once the policy matures. Or when a friend boasts that he made a killing in the commodities but you are sticking to same boring once in a month SIPs. Being Dhoni is very tough but it’s worth when you get a World Cup.

And now the last one but I feel it to be the most important:

Attitude: We all know how last year went for Yuvraj. Out of the team and people started talking about his pot belly, party animal nature etc. But after World Cup win, Yuvi said in an interview to TOI, that “if next time I am out of form, do not blame my lifestyle”…. That’s a winner’s attitude. When you have a point to prove, prove it and point it to the world. In Yuvi language – Let “balla” do the talking. In your financial life other people will not forget or forgive your bad decisions. Do not fight with a pig as it is the pig that enjoys a mud fight, but you get dirty in the bargain. Best way is to reenergize and stick to the basics. Once you are successful, show it to the world as after a criticism session you deserve an applause too.

They say “learn a good thing from your religion” so we should also learn from cricket as “Cricket is not less than a religion in India”.

Would you like to add few more finance related learnings from cricket?? 🙂

Just one word – investment?? And your response will be that you have been doing it since you were wearing half pants or a frock. Remember how you always managed your personal budget with your pocket money. You saved in earthen pots and pig faced reservoirs. Remember the piggy banks? But again was this money enough? No. It was not as this was saving and not investment.

Saving will not result in wealth creation. Our piggy banks never contributed even a rupee to our wealth. Money was idle but not growing. But is money a tree which grows by itself? Yes. Money can grow on its own, provided it gets a balanced climate and the environment it requires. A tree requires sunlight, water and minerals, investments also need a few essentials to grow. And with the right amount of these, it needs time to show its true colors. Few things like growth and character need time to develop and so do investments. They also need time and patience to bear fruit.

Let’s check this infographic – 10 Commandments of Investing – may help you in growing your money tree. (if you like this, must share with your friends)

Which is the Mutual Fund for ELSS or which is the best Mutual Fund for SIP or which is the best term plan? This is the most common trick to ask secrets from Hemant. 🙂 And as usual my answer is “There is nothing called best – best comes after postmortem”.

But won’t you like to ask what happened if someone made investments when the sensex touched its highest point in last bull run. If someone had invested Rs 10000 in ELSS Fund on 9th January 2008 (Sensex 20800) & withdrawn it after 3 years on 10th Jan 2011 (luckily Sensex 19100).

So couple of funds have given negative returns in this period & if you notice in middle of this period funds even lost almost 50% of their value. Equity is the most volatile asset class & it always work like this – if you don’t have risk appetite or if you want that your investments should never go negative, please don’t invest in equity or equity related instruments.

So we have seen a single period but this cannot be much helpful in any judgment. Let’s see what happened in all 3 year periods since ELSS came to existence – for that we have to understand rolling returns.

Definition of Rolling Returns: The annualized average return for a period ending with the listed year. Rolling returns are useful for examining the behavior of returns for holding periods similar to those actually experienced by investors.

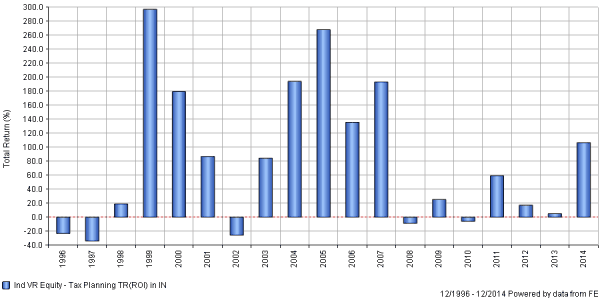

3 year rolling return of ELSS

For example, the three-year rolling return for 1996 covers Jan 1, 1993, through Dec 31, 1996. The three-year rolling return for 1996 is the average annual return for 1993 through 1996.

So you can see there are couple of negative periods here – all 3 year period that are starting from a peak of bull market. Deepest fall, almost a 30% negative in 1997 because this is talking about investments done at the time of Harshad Mehta’s Scam (1993).

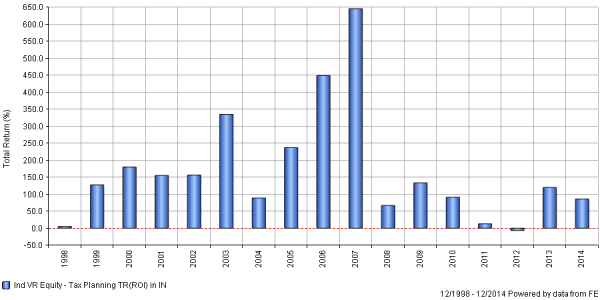

If we look at 5 year period there is only 1 negative period – ending 2012. If you do a Prima Facie observation – on an average investments has given more than 100% return or doubled in period of 5 years.

If you look both the rolling charts there are a two important learning:

First, with increase in investment horizon (3 to 5 years) volatility substantially reduces.

Second, investments done when actual returns were negative have generated a good return. (Check 3 year period)

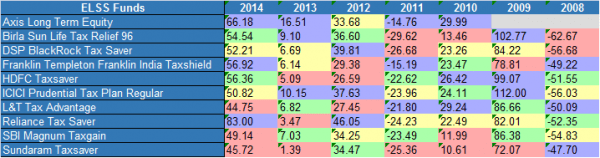

This is just a list of 10 tax saving mutual funds – you can take a decision with your own research. (Top 10 ELSS funds based on assets under management)

Long term Performance of ELSS Funds (absolute return)

Source: IMF

Source: IMF

His AMC managed only single fund – PPFAS Long Term Equity Fund – no other equity or even debt fund. And no plan to launch second equity scheme. In a previous interview, he said Asset Management is not a grocery store business. There is just one single way to right investing. You can’t have 20 ways.

His AMC managed only single fund – PPFAS Long Term Equity Fund – no other equity or even debt fund. And no plan to launch second equity scheme. In a previous interview, he said Asset Management is not a grocery store business. There is just one single way to right investing. You can’t have 20 ways.

")