Last Updated on April 10, 2026 by teamtfl

In my 25 years of financial planning, some client conversations stay with me longer than others.

A father who came to me in 2012. His son was 9 years old, had cerebral palsy, and would need lifelong care. The father was 44. His question was simple: “If something happens to me and my wife, what happens to him?”

He did not have an answer. Neither did his lawyer. Neither did his CA. Nobody had thought about it in a structured way.

That conversation shaped how I think about financial planning for families with special needs dependents. This is not normal family planning with a few extra line items. It is a fundamentally different challenge — planning across two generations, with a level of emotional and financial complexity that most advisors are not equipped to handle.

⚡ Quick Answer

Financial planning for families with special needs children involves planning for the child’s lifelong care beyond the parents’ lifetime — covering corpus creation, trust structures, guardianship, government scheme benefits (like NHFDC), and estate planning. Jitendra Solanki’s book “Financial Planning for Families Having Children with Special Needs” is the first comprehensive Indian guide on this topic and is essential reading for any such family or advisor serving them.

Why This Is a Different Planning Problem

In standard family financial planning, the life map looks predictable: save for education, support career launch, fund your own retirement, leave an estate. Once children are independent, the parents’ planning focuses on themselves.

For a family with a special needs dependent, this map does not apply. The dependent will need care for their entire lifetime — which will likely outlast the parents. That creates a planning problem with two simultaneous horizons:

Horizon 1: The parents’ lifetime — earning, saving, building the corpus, managing current care costs, maintaining insurance, planning for income shocks.

Horizon 2: After the parents — who provides care, who manages funds, how are funds protected from misuse, what legal structures ensure the dependent’s security.

Most financial advisors in India are equipped to plan Horizon 1. Very few have the knowledge, sensitivity, and specialisation to address Horizon 2.

The Book: A Review

Jitendra P.S. Solanki wrote “Financial Planning for Families Having Children with Special Needs” — the first book published in India on this specific subject. Jitendra runs a niche financial planning practice at PlanSpecialNeeds.com exclusively for these families. His wife Dr. Shweta is an occupational therapist who works with special needs children — which means the book reflects both the financial and the lived reality of these families.

I have worked with special needs families directly, so I can say with confidence: this book fills a genuine gap. It is not a theoretical text. It is a practical guide that answers the question every such family eventually asks — “Where do we even start?”

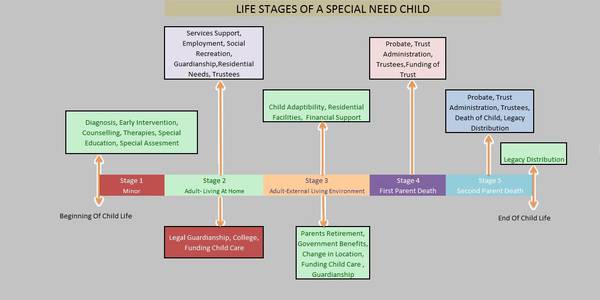

The book is structured around the life stages of a special needs child — from diagnosis, through childhood care, into adulthood, and ultimately addressing what happens after the parents are no longer present. Each stage brings specific financial, legal, and emotional challenges that the book addresses clearly.

The chapters on estate planning — Will, Trust, Guardianship — are particularly valuable. These are areas where most families have enormous anxiety and very little clarity. The book explains them accessibly, without legal jargon, in the Indian context.

The real-life family case studies are what elevate this book above a standard financial planning text. The emotional reality of these families — the grief, the hope, the daily uncertainty — is documented honestly alongside the financial frameworks.

Are you planning for a family with a special needs dependent?

This requires specialised financial planning that most advisors do not provide. We can help you think through the two-generation planning challenge.

Key Planning Principles for Special Needs Families

For families navigating this situation, here are the foundational planning principles that every advisor and family should understand:

1. Build a “Special Needs Trust” (or equivalent structure)

A direct bequest to a special needs dependent can inadvertently disqualify them from government benefits they are entitled to. A trust structure ensures the funds are available for the dependent’s care without affecting their eligibility for social welfare schemes. The trust must be professionally drafted with a clear mandate for the trustee.

2. Appoint a guardian explicitly

The guardian is the person who will make care decisions for the dependent after the parents are unable to. This person must be identified, willing, and legally appointed — not assumed. The legal process for guardianship under the National Trust Act (1999) must be followed for families with dependents who have autism, cerebral palsy, mental retardation, or multiple disabilities.

3. Know your government entitlements

India has a range of schemes for families with special needs dependents that are significantly underutilised: National Handicapped Finance and Development Corporation (NHFDC) loans, Niramaya health insurance scheme, ADIP (Assistance to Disabled Persons) scheme, and various state-level benefits. The National Trust Act provides for registration and guardianship. These are legal entitlements — not charity.

4. Separate the “care corpus” from retirement savings

The corpus required for the dependent’s lifelong care must be built separately from your retirement savings. Mixing them creates a situation where drawing down one impairs the other. Goal-based financial planning is the only framework that handles this correctly.

5. Plan for income interruption

Parents of special needs children are statistically more likely to face career interruptions — one parent may reduce working hours or stop entirely to manage caregiving. Disability insurance, term insurance with higher covers, and emergency fund discipline are not optional in these families. They are existential.

Where to Get the Book

The book is available on Amazon India and leading bookstores. If you know a family navigating this situation, this is one of the most genuinely useful gifts you can give them. If you are a financial advisor, this is required reading.

The financial planning challenge for families with special needs dependents is one of the most complex and emotionally charged problems in personal finance. It deserves specialised attention — not a standard financial plan with a few adjustments. If you are in this situation, please do not face it alone.

Planning for 2 generations requires a different kind of advisor, a different kind of plan, and a different kind of urgency. Start now.

💬 Your Turn

If you are a parent of a special needs child, or a financial advisor who has worked with such families, please share your experience in the comments. What was the hardest planning question to answer? What resources did you find most useful? This conversation can help families who are just starting this journey.