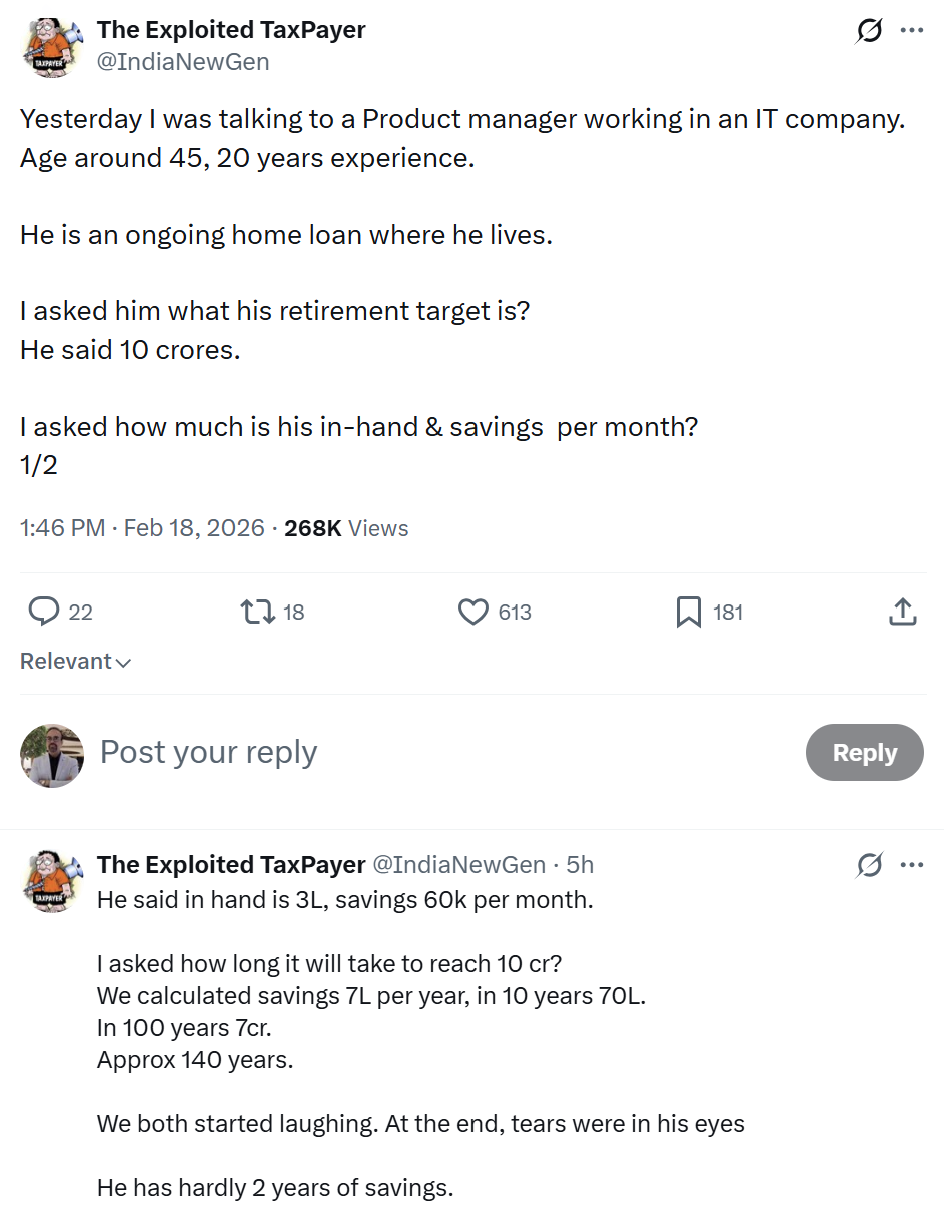

Yesterday, a Twitter thread went viral.

45-year-old product manager in an IT company with ₹3 lakh in-hand salary and 20 years of experience

Retirement target: ₹10 crore

Monthly savings: ₹60,000.

When someone did the math for him, he started laughing. Then there were tears.

Because the numbers showed something he’d been avoiding for years: at his current savings rate, he’d reach ₹10 crore in approximately 140 years.

He has 15 years until retirement.

This isn’t a story about one person.

This is the story of middle-class India — and the harsh truth about retirement planning in India.

8 Facts About Retirement Planning

The Aspiration–Execution Gap in Retirement Planning

We’ve all seen retirement calculators in India.

Punch in some numbers. Get a target retirement corpus. Feel momentarily anxious. Close the tab.

₹5 crore. ₹8 crore. ₹10 crore.

These numbers float around in our heads as vague targets — “somewhere around there should be fine.”

But here’s what I’ve learned after reviewing hundreds of retirement plans: most people treat their retirement number like a wish, not a plan.

They know the destination. They have no idea what the monthly ticket costs.

A ₹10 crore retirement corpus in India at age 60 sounds reasonable if you’re 45 and earning well.

But reasonable and achievable are not the same thing.

The gap between “I want ₹10 crore” and “I’m saving ₹60,000 a month” is where retirement savings gaps quietly grow.

The Math Nobody Wants to Do

Let me show you what ₹60,000 per month actually becomes.

Assume you’re 45. You have 15 years until 60.

Assume a consistent 12% annual return (which is optimistic for a balanced portfolio as you near retirement).

₹60,000 monthly SIP for 15 years = approximately ₹2.5 crore.

Not ₹10 crore. Not even close.

To reach ₹10 crore in 15 years at 12% returns, you’d need to save roughly ₹2.4 lakh per month.

Four times what he’s currently doing.

And that’s assuming no market crashes, no job loss, no medical emergencies, and a disciplined 12% return every single year.

The brutal truth? Most people in their 40s are tracking toward 20-30% of what they actually need.

Not because they’re irresponsible.

Because they started late, and nobody showed them the real math.

The Home Loan Trap and Its Impact on Retirement Savings

Here’s the part that makes this worse.

The 45-year-old in that thread? He has an ongoing home loan.

This is the Indian middle-class script:

Age 28-32: Get married, buy a house, take a 20-year loan.

Age 32-45: Pay EMI religiously. Feel like you’re “investing.”

Age 45: Realize the EMI ate your prime compounding years.

Age 48: Start panicking about retirement.

A ₹50 lakh home loan at 8.5% interest over 20 years costs you roughly ₹80 lakh in total payments.

That ₹30 lakh in interest? That’s ₹30 lakh that didn’t compound in your retirement corpus.

I’m not saying don’t buy a home.

I’m saying the home loan delay is why most people reach 45 with ₹2-3 lakh saved instead of ₹50-60 lakh.

And once you’re 45 with ₹2 lakh saved and ₹10 crore needed, the math stops being forgiving.

What To Do After Retirement in India ?

The Recalibration Nobody Wants in Late Retirement Planning

So what does this 45-year-old do now?

He has three options. None of them are comfortable.

Option 1: Radically increase savings rate.

Cut lifestyle. Delay purchases. Push monthly savings from ₹60k to ₹1.5-2 lakh. Possible? Maybe. If both spouses work. If kids are done with expensive school years. If there’s zero lifestyle creep.

Realistic? For most people, no.

Option 2: Extend working years.

Don’t retire at 60. Work till 65. Maybe 67.

Buys you more earning years, more compounding years, and fewer withdrawal years.

The math works. The reality is harder. Not everyone’s body cooperates. Not every industry keeps you past 55.

Option 3: Redefine retirement.

This is the one nobody wants to hear, but it’s the most honest.

If ₹10 crore isn’t reachable, what is?

Maybe ₹4 crore is reachable. What does retirement look like on that?

Smaller house. Tier-2 city instead of metro. Simpler lifestyle. No foreign vacations.

Not a failure. Just a recalibrated reality.

The mistake isn’t ending up with ₹4 crore instead of ₹10 crore.

The mistake is reaching 58 still believing you’re on track for ₹10 crore when you’re not.

WHAT I’VE LEARNED IN 25 YEARS

I’ve had this exact conversation — the laughing that turns into tears — more times than I can count.

And here’s the pattern:

The people who sleep well at night did the uncomfortable math at 35.

The people who panic did the math at 50.

Same math. Different outcomes.

Because at 35, you still have options. The compounding window is open. Small course corrections create big results.

At 50, you have options too. Just harder ones.

The gap between aspiration and execution doesn’t close by itself.

It closes when you stop guessing and start calculating your real retirement corpus requirement.

Not someday.

Today.

Because 140 years is a long time to wait for ₹10 crore.